Consolidation Loans: A 2026 Guide to Simplifying Your UK Finances

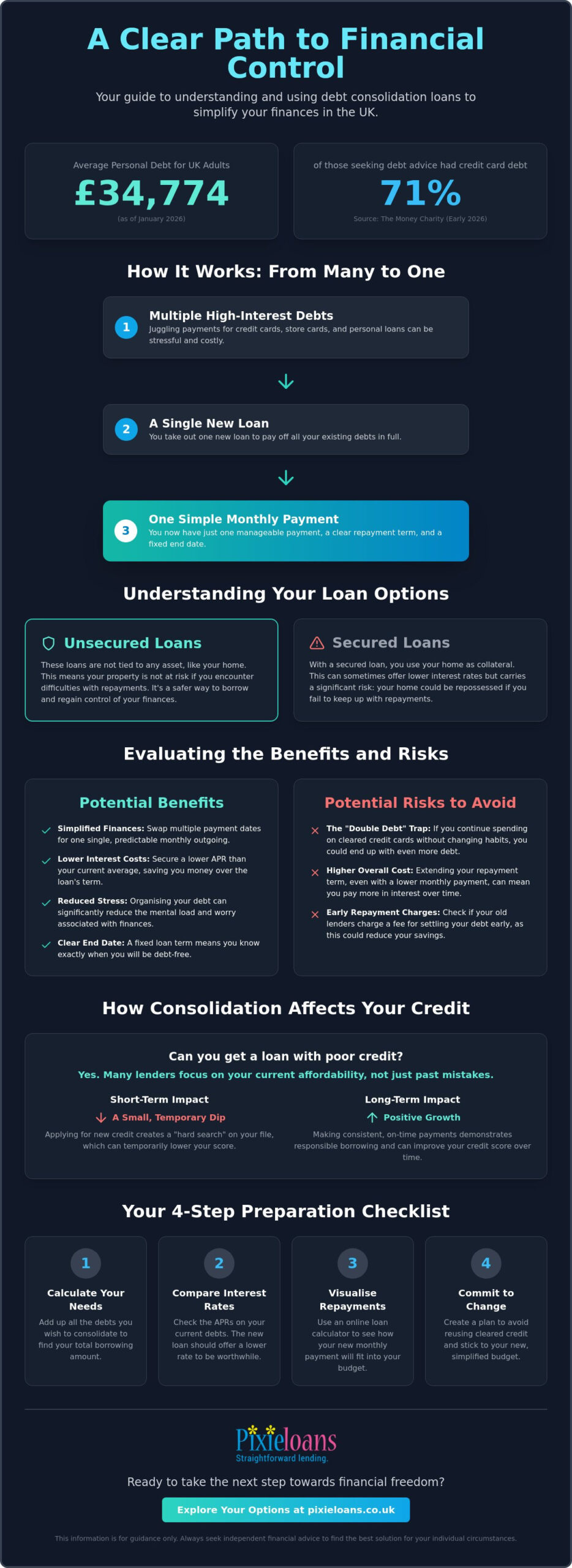

Did you know that by January 2026, the average personal debt for adults in the UK reached £34,774? If you feel overwhelmed by high interest rates or the worry of missing a payment date, you aren’t alone. Many people use consolidation loans to simplify their monthly outgoings and regain control. It’s a practical way to handle your finances and reduce the daily stress of managing multiple creditors.

This guide explains how these loans work by merging your debts into one single, lower monthly payment with a clear end date. We’ll explore the latest 2026 market trends, such as representative APRs from lenders like Santander at 6.4%. You’ll learn to evaluate the benefits and risks whilst discovering tips to streamline your finances. By the end, you’ll have a straightforward plan to organise your repayments more effectively.

According to the Financial Conduct Authority, there’s an increased focus on supporting consumers with suitable debt products this year. Recent data from The Money Charity shows that 71% of people seeking debt advice in early 2026 had credit card debt. These insights help ensure you make an informed choice for your financial future.

Key Takeaways

- Understand the simple mechanism of merging several debts into one clear monthly balance.

- Explore the potential to lower your overall interest rates and set a definite end date for your debt.

- See how consolidation loans work for different credit scores and what impact they might have on your credit file.

- Follow our practical checklist to prepare your application and accurately calculate your total borrowing needs.

- Learn how to use online tools to visualise your new repayment schedule before you commit to a plan.

What are consolidation loans and how do they work in the UK?

A debt consolidation loan is a single new loan you take out to pay off multiple existing debts, like credit cards or store cards. The process for consolidation loans is simple: you receive the funds, use them to clear your other balances, and then have just one monthly repayment to manage. In the UK, these are usually unsecured personal loans. According to StepChange, this is a popular way to regain financial control. To understand the basics, you might ask, what is debt consolidation? It’s essentially a strategy to simplify your life.

The difference between secured and unsecured options

Unsecured loans don’t require your home as collateral, whilst secured loans do. This means if you struggle with repayments on a secured loan, your property could be at risk. Pixie Loans focuses on unsecured options because we believe in keeping your home safe from the borrowing process. Before you apply, check the interest rates on your current cards and loans. If the new loan’s rate isn’t lower than your current average, it might not be the best move. Always compare your options carefully to ensure you’re actually saving money on interest.

Key terminology you need to know

APR stands for Annual Percentage Rate. It shows the total cost of borrowing, including interest and fees. As of June 2026, representative APRs for unsecured consolidation loans range from 5.9% to 6.5% for good credit. The “term” is how long you have to pay it back. One UK debt expert states, “The total repayable amount is the most honest figure in any agreement.” To see how different terms affect your budget, you can use our calculator. This aligns with the FCA focus on consumer support.

Evaluating the benefits and risks of consolidating your debt

Reducing the mental load of debt is just as important as the financial saving. When you use consolidation loans, you swap multiple confusing payment dates for one favourite day each month. This organisation often leads to a significant drop in stress levels. Data from the Money and Pensions Service shows that the average Brit is estimated to have £1,400 of credit card debt in 2026. By securing a lower interest rate than your current cards, you can save money, but you must weigh up the advantages and disadvantages of consolidation carefully.

When is a consolidation loan the right choice?

This path is ideal if you have a stable income and a clear budget. You should use a loan calculator to compare your current monthly total against the proposed new repayment. If the new payment is lower, it provides immediate breathing room. However, consolidation loans only work effectively if you commit to stop using the credit cards you’ve cleared. To start your journey, you can view our simple application form to see your options. This ensures your debt actually disappears rather than just moving around.

Potential pitfalls to avoid

The biggest danger is “double debt.” This happens if your spending behaviour doesn’t change after clearing your cards. You should also watch out for early repayment charges (ERCs). Some existing lenders charge fees for closing accounts early, which could eat into your savings. Whilst waiting for approval, try a “no-spend week” to organise your budget. This practical step helps you adjust to your new financial structure. If you extend your loan term significantly, you might pay more interest over time, even if the monthly rate is lower.

Eligibility and how consolidation loans affect your credit

Many people worry that a low credit score stops them from getting help. Can you get a loan with poor credit? Yes, you can. Specialist lenders in the UK often look at your current affordability rather than just your past mistakes. This is important as individual insolvencies rose by 20.4% in the first quarter of 2026. When you take out a new loan, your credit score might see a small, temporary dip. This happens because lenders perform a “hard search” on your file. However, making consistent on-time payments is great for your long-term credit behaviour. For more details, read about Bad Credit Consolidation Loan Lenders to find the right fit for 2026.

Understanding the role of a credit broker

We act as a bridge between you and a wide panel of lenders. Pixie Loans uses “soft search” technology to check your eligibility. This means you can see your chances of approval without hurting your credit score. It’s vital to be honest on your application. Providing accurate figures for your income and outgoings helps us find a match that fits your budget. We’re a broker, not a direct lender, which you can learn more about on our About Us page.

Steps to improve your eligibility today

You can take simple steps to boost your chances right now. First, check that you’re on the electoral roll. Lenders use this to verify your home address quickly. Next, review your credit report for any errors. Even a small mistake in your address can cause a rejection. You should also try to reduce your credit utilisation ratio by paying down small balances where possible. For a deeper look at your options, check our consolidation loans guide. If you feel ready to see what’s available, start your application today to explore your personalised offers.

How to prepare and apply for a consolidation loan

Preparing for consolidation loans is all about precision. You aren’t just moving money; you’re building a new financial habit. First, calculate the exact total needed to pay off your debts. Don’t guess; check your latest statements. Next, use the Pixie Loans calculator to see if the monthly repayments fit your 2026 budget. Gather your income details and creditor names before you start. Finally, complete the online application form to see your matches. Being accurate now makes the process much smoother later.

What to expect after you apply

Decision times vary. Many lenders offer a result quickly, whilst others take a few days to review your details. If you’re declined, don’t apply elsewhere immediately. This can hurt your credit score. Instead, take a breath and seek advice. You can also read our guide on how to consolidate credit card debt with bad credit. This resource helps you understand your next steps. Remember, a rejection isn’t the end of the road; it’s just a sign to review your plan.

Expert tips for a successful financial recovery

Staying organised ensures long-term success. One financial expert says, “Setting up a Direct Debit for your new loan is the best way to stay organised and avoid late fees.” Once your old accounts are paid off, close them to avoid the temptation to spend. This simple action protects your progress. For further official guidance on managing your debts, visit GOV.UK. These steps help you move from managing debt to total financial freedom. You’ve got the tools; now it’s time to use them.

Take control of your financial future today

Managing your money shouldn’t feel like a constant battle against calendar dates and high interest rates. By choosing consolidation loans, you can transform a complex web of debts into one manageable monthly payment. We’ve explored how this strategy helps you stay organised and potentially reduces the total cost of your borrowing. It’s vital to always compare the APR and total repayable amount to ensure your new plan fits your long-term goals and daily budget.

At Pixie Loans, we act as your pragmatic facilitator. Our quick online matching process connects you to a panel of specialist UK lenders without any hidden fees. This approach allows you to explore your options with transparency and confidence. If you’re ready to simplify your outgoings and work towards a clear end date for your debt, now is the time to act. Taking this step can provide the breathing room you need to focus on what matters most in your life.

Check your eligibility for a consolidation loan today and start your journey towards better financial health. You have the power to organise your finances and reduce daily stress. We’re here to help you bridge the gap to a more predictable and manageable future. You’ve got this.

Frequently Asked Questions

Will a consolidation loan lower my monthly payments?

Yes, a consolidation loan can lower your monthly payments by securing a lower interest rate or extending the repayment term. For example, if you move high-interest credit card balances to a loan with a 6.4% representative APR, your monthly outgoings will usually drop. You must be careful, however; if you choose a much longer term to make payments smaller, you might pay more interest in total over the life of the loan.

Can I get a consolidation loan if I have a bad credit history?

Yes, you can still apply for consolidation loans even if you have a poor credit history. Specialist lenders often prioritise your current income and regular outgoings over past credit mistakes. They want to see that you can afford the new monthly repayment comfortably right now. Whilst your options might be more limited than someone with a perfect score, many lenders on our panel focus on helping people rebuild their financial health. Our guide on how to get a debt consolidation loan with bad credit explains how to match your financial profile with the right specialist lender.

Is it better to use a credit broker or go directly to a bank?

Using a credit broker is often better if you want to compare multiple lenders at once without several hard searches on your file. A bank only offers its own products, which might not be the most competitive for your specific needs. As a broker, we act as a facilitator, matching you with a variety of specialist UK lenders. This saves you time and helps you find a more suitable deal for your circumstances.

What happens if I cannot afford the repayments on my new loan?

If you find you can’t afford a repayment, you should contact your lender immediately to discuss your options. They are required by the Financial Conduct Authority to treat customers fairly and may offer a temporary payment plan. You can also seek free, confidential help from organisations like National Debtline. It’s best to act quickly before you miss a payment and damage your credit score further.

Are there any hidden fees when using a broker for a consolidation loan?

No, there are no hidden fees when you use Pixie Loans to find consolidation loans. We are transparent about our role as a broker; we receive a commission from the lender if your application is successful, so we don’t charge you a penny for the service. This means the matching process is free for you to use. You’ll always see the full breakdown of costs and interest from the lender before you sign any agreement.