How to Get a Debt Consolidation Loan with Bad Credit in the UK (2026)

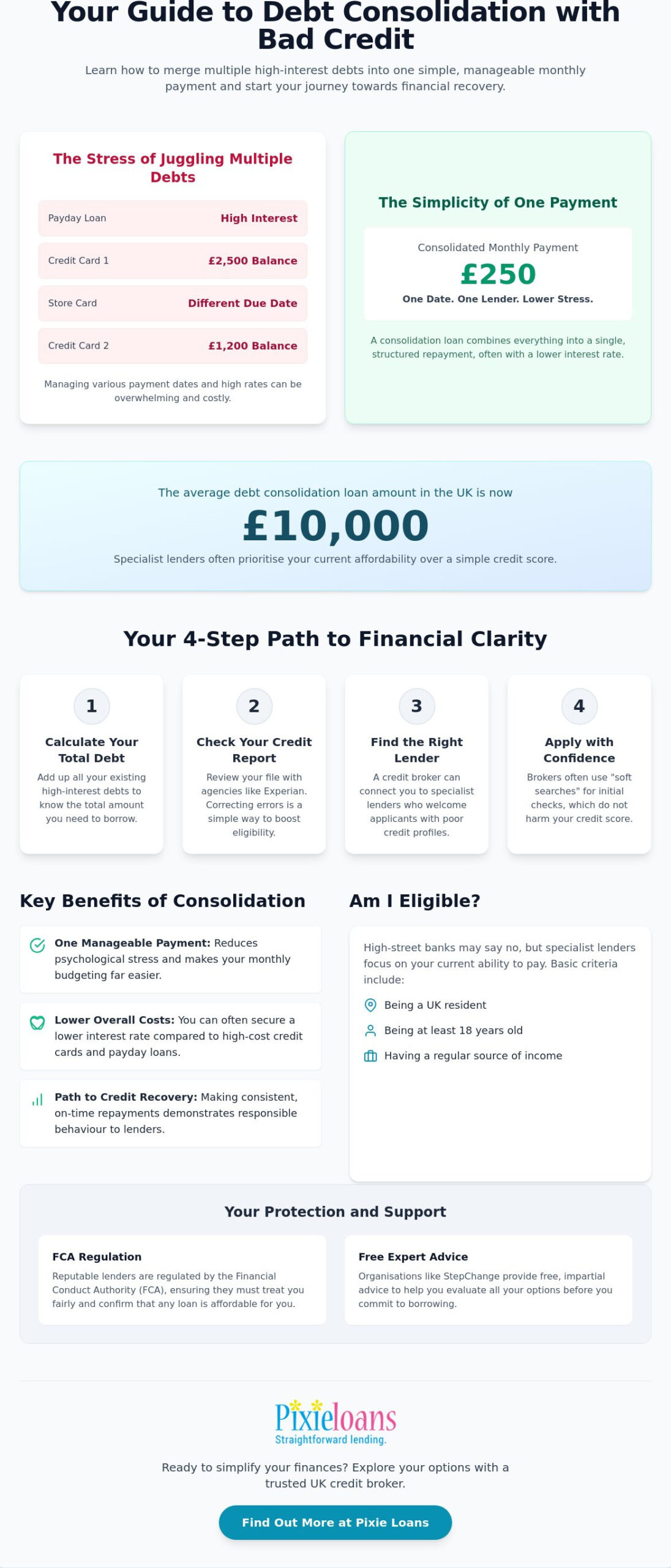

Did you know that the average debt consolidation loan in the UK is now £10,000? If you are currently managing multiple high-interest payday loans or credit cards, then you likely understand the stress of juggling different payment dates. It is a common worry that a poor credit history will lead to automatic rejection from high-street banks. However, securing a debt consolidation loan bad credit solution is often a matter of matching your specific financial behaviour with a specialist lender that values affordability over a simple score.

This guide will show you how to simplify your outgoings into one manageable payment and start your path toward credit recovery. We will examine how Financial Conduct Authority regulations are designed to ensure lenders act in your best interest. If you follow these practical steps, you can reduce monthly costs and find a structured way to improve your financial health. For those who need support, organisations like StepChange provide free advice to help you evaluate your options before you borrow.

Article Summary

Merge Your Debts

Learn how a debt consolidation loan bad credit option can help you merge multiple high-interest debts into a single, manageable monthly payment. This tool is designed for individuals with defaults or lower scores who want to simplify their finances and reduce the stress of multiple payment dates.

Eligibility Criteria

Discover why specialist lenders prioritising affordability may offer support even if high-street banks have said no. With the average debt consolidation loan amount in the UK being £10,000, the Financial Conduct Authority ensures lenders focus on your current ability to repay rather than just a historic number.

Practical Steps

Follow a clear path by calculating your total debt and checking your credit report through Experian. Identifying errors on your report is a simple way to boost your eligibility before you apply. You can also check Equifax to ensure all your records are accurate across different agencies.

Long-Term Recovery

Understand how to use your new loan as a fresh start for your credit score. By making consistent, on-time repayments, you can demonstrate responsible financial behaviour and work towards a more stable future whilst avoiding the need for further borrowing or high-interest credit products.

What is a Debt Consolidation Loan for Bad Credit?

A debt consolidation loan bad credit option is a financial tool designed to merge multiple high-interest debts into one manageable monthly instalment. In 2026, as living costs continue to rise across the UK, many households use these loans to regain control of their monthly outgoings. You don’t need a perfect credit score to apply; these products are specifically tailored for individuals with past defaults or low scores. If you’ve wondered what is debt consolidation?, it’s simply the process of taking out one new loan to pay off several smaller, more expensive ones.

How Consolidation Works for UK Borrowers

The process involves transitioning from paying several different creditors to paying just one specialist lender. These lenders are regulated by the Financial Conduct Authority to ensure they follow strict rules on affordability and fair treatment. You generally have two main choices: unsecured loans, which don’t require collateral, or secured loans, which are tied to an asset like your home. Specialist lenders often focus on your current ability to keep up with repayments rather than just looking at a number on a credit report. This approach makes borrowing more accessible for those with a complex credit history.

The Benefits of Simplifying Your Outgoings

Managing just one payment date instead of five significantly reduces psychological stress and makes budgeting much easier. You’ll likely find that the interest rate on a consolidation loan is lower than the rates on payday loans or credit cards, which helps you save money over time. By reducing your monthly outgoings, you create more breathing room in your budget for everyday essentials like groceries and bills. This structured approach helps you stop the cycle of borrowing and starts you on a path toward long-term financial stability and credit score recovery.

Evaluating Your Eligibility and Finding the Right Lender

To qualify for a loan, you must meet a few basic criteria. You need to be a UK resident, at least 18 years old, and have a regular source of income to cover your repayments. While high-street banks often focus on a rigid credit score, specialist lenders prioritise your current affordability. They look at your monthly budget to ensure you can comfortably meet the new instalment. This is particularly helpful when seeking a debt consolidation loan bad credit solution, as it shifts the focus from past mistakes to your present financial health.

Many applicants worry that applying will damage their credit score further. Most reputable brokers use “soft searches” during the initial matching phase. These searches allow lenders to check your eligibility without leaving a visible mark on your credit file. If you’re unsure about your next steps, reading about managing your debt consolidation loan from charities like StepChange can provide extra clarity. Representative APRs for these specialist loans can range from 14% to over 40%, so it’s always wise to compare the total cost of borrowing.

The Broker Advantage for Poor Credit Profiles

Finding the right lender is much easier when you use a credit broker. Instead of applying to multiple companies individually, a broker connects you to a panel of lenders with different risk appetites. This saved time is vital if you have CCJs or defaults on your record. By using a service like Pixie Loans, you can filter for lenders who specifically accept applicants with poor credit profiles. This process helps you avoid unnecessary rejections that could harm your credit file.

Specialist Lenders vs. High-Street Banks

High-street banks often have a “tick-box” approach that leads to quick rejections for anyone with a less-than-perfect history. In contrast, specialist firms take a more flexible view. They often focus on your financial behaviour over the last 12 months rather than looking back several years. For a deeper look at these providers, see our guide on bad credit consolidation loan lenders. If you feel ready to see which options are available for your circumstances, you might consider starting a quick online application today.

Step-by-Step Guide to Consolidating Your Debt

Taking control of your finances requires a clear, methodical plan. Start by listing every debt you currently owe, including the balance and the interest rate. You can then use a loan calculator to see what a new monthly instalment might look like. It’s also vital to check your credit report through Experian or Equifax to identify any errors. If you find a mistake, correcting it could improve your eligibility for a debt consolidation loan bad credit agreement before you even apply.

Once your data is ready, submit a single application through a broker to view multiple options from specialist lenders. This approach prevents you from making too many individual applications, which can hurt your credit score. Compare the Annual Percentage Rates (APRs) and the total cost of the loan carefully. After you finalise the agreement and receive the funds, ensure you pay off your old high-interest debts immediately. This prevents the risk of falling back into a cycle of multiple payments.

Calculating Your Total Debt and Affordability

To find the right loan, you need to know exactly where your money goes. List every creditor and interest rate to determine your total requirement. Be realistic about your monthly budget, ensuring you leave enough for essentials like food and energy bills. If you aren’t sure if you qualify, visit the emergency loans eligibility page to check the basic criteria. Understanding your affordability today is the best way to ensure a successful financial recovery tomorrow.

Completing the Application and Comparing Offers

When you fill out your application, honesty is the best policy regarding your income and outgoings. Lenders use this information to decide if a loan is suitable for your specific circumstances. Look beyond the monthly cost and check for any hidden fees or early repayment charges in the agreement. This ensures you aren’t surprised by extra costs later on. If you feel prepared to simplify your outgoings, you can start your journey by completing the application form right now.

Managing Your New Loan and Rebuilding Your Credit

Think of your debt consolidation loan bad credit agreement as a clean slate for your finances. It’s a fresh start, not an excuse to take on more debt. By making consistent, on-time repayments, you’ll show lenders that your financial behaviour has improved. This is the most effective way to see a positive impact on your credit score over time. To ensure you never miss a date, set up standing orders for your monthly instalment. It’s also a good idea to close old credit card accounts once they’re paid off to avoid the temptation of spending again.

Long-term Financial Health and Behaviour

Building a small emergency fund whilst repaying your loan is a smart move. Even saving a few pounds a week can help you handle unexpected costs without needing new credit. Reducing your “credit utilisation” ratio, which is the amount of credit you use compared to your limit, also helps boost your score. For specific tips on dealing with card balances, read our guide on how to consolidate credit card debt with bad credit. New Buy Now Pay Later regulations from July 2026 offer even more protection for UK borrowers.

What to Do if Your Circumstances Change

If your circumstances change, talk to your lender immediately. Under the FCA Consumer Duty, lenders must support you if you’re struggling. They might provide a temporary payment plan or breathing space. Recent consultations like CP26/18, running until 28 July 2026, show a push for even better support for underserved borrowers. Pixie Loans acts as a responsible guide throughout your journey. For free advice, visit MoneyHelper. Being proactive is the best way to protect your financial health and your future credit score.

Take Control of Your Financial Future Today

Securing a debt consolidation loan bad credit solution is a practical step toward simplifying your daily life. By merging expensive balances into one monthly instalment, you can reduce mental stress and start the process of rebuilding your credit score through consistent repayment behaviour. Remember that specialist lenders who prioritise affordability give you a genuine chance to move forward, even if high-street banks have previously said no. This structured approach helps you stop the cycle of borrowing and focus on long-term stability.

As an FCA-authorised credit broker, Pixie Loans offers a transparent matching process with no hidden fees. We provide access to a wide panel of specialist lenders who understand that your financial history doesn’t define your future. If you feel ready to organise your outgoings and find a more manageable path for your household budget, we’re here to support you every step of the way.

Apply for a debt consolidation loan today and simplify your finances. You now have the knowledge and the tools to create a more stable financial future; it just starts with one small, positive decision.

Frequently Asked Questions

Can I get a debt consolidation loan with a CCJ in 2026?

Yes, you can still obtain a loan if you have a County Court Judgment (CCJ) on your record. Specialist lenders look beyond your historic credit file to assess your current affordability and income stability. Under the Financial Conduct Authority’s Consumer Duty, these lenders must ensure their products are suitable for your specific needs. Whilst a CCJ stays on your file for six years, showing recent responsible behaviour with your other bills helps your application succeed.

How much can I borrow for debt consolidation with poor credit?

You can typically borrow between £1,000 and £50,000, though the average debt consolidation loan bad credit amount is approximately £10,000. For unsecured loans, your regular income and monthly outgoings determine the final limit. Most borrowers choose a repayment term of around five years to keep the monthly instalments manageable. If you need a larger amount than £50,000, you might need to consider a secured loan using your home as collateral.

Will a debt consolidation loan hurt my credit score?

An initial application through a broker won’t hurt your score because they use soft searches, but the final hard search by a lender might cause a temporary dip. In the long run, consolidating your debts usually helps your credit profile. By merging several high-interest accounts into one, you lower your overall credit utilisation. If you consistently make every payment on time, you’ll demonstrate the reliable behaviour that future lenders want to see on your report.

What is the typical interest rate for bad credit consolidation loans?

Interest rates for these loans vary significantly, often ranging from 14% to over 40% depending on your circumstances. Some specialist lenders have representative APRs as high as 99.9% for high-risk applicants. Whilst the average APR for a standard consolidation loan is 15.8%, you should expect to pay more if your credit history is poor. It’s essential to check the total cost of borrowing, including all fees, before you sign any agreement.

What happens if I am rejected for a debt consolidation loan?

If you’re rejected, you shouldn’t submit another application immediately, as multiple hard searches in a short time can damage your score. Instead, you should check your credit report for errors and wait at least six months before trying again. It’s also a good idea to seek free support from organisations like MoneyHelper. They can help you explore other ways to manage your debt whilst you work on improving your eligibility.