Quick £200 Loan Guide: Easy Steps to Apply & Get Approved Today

Estimated reading time: 12 minutes

Takeaways

- A Quick £200 Loan helps cover unexpected expenses and usually doesn’t require collateral.

- The application process is simple, allowing quick access to cash without extensive paperwork.

- Eligibility criteria typically include being over 18, a UK resident, and having a regular income.

- Repayment options vary, and many loans allow early payments without extra fees, helping to save on interest costs.

- Using automatic payments can prevent missed deadlines and promote a good credit history.

Table of contents

Are you looking for a quick £200 loan for an unexpected bill? Most personal loans range from £1,000 to £25,000, which makes smaller amounts tough to get through regular channels. Specialised lenders now step in to help bridge these financial gaps.

Firstly, a £200 loan from a direct lender works quite differently than larger personal loans. Most high-street personal loans are unsecured, so you don’t need to put up valuable assets like your home as collateral.

Secondly, the sort of thing we love about small loans is their simple application process. This makes them different from larger loans that need lots of paperwork. You should think over your options carefully, whether you want a £200 payday loan or you’re learning about £200 loans with bad credit.

Here’s what you need to know to get this financial boost quickly and responsibly.

Understanding how a £200 loan works

In short, a £200 loan could help you deal with a small money emergency. Let’s look at what these loans are and how they work before you submit your application.

What is a £200 personal loan?

As can be seen, a £200 loan serves as a small, short-term borrowing option that helps cover surprise expenses or money gaps between paydays. These loans give you quick cash relief when unexpected costs pop up.

Most £200 loans are unsecured, so you won’t need collateral or someone to back your loan, which helps if your credit isn’t perfect. Lenders review your application based on your income and how you’ll pay it back.

People use a £200 loan to:

- Fix their car and stay mobile

- Pay surprise household bills or emergency costs

- Make small home fixes or needed repairs

- Cover gaps between paychecks when surprise bills show up

In addition, some people refer to these as payday loans. A £200 loan can take different forms, including short-term installment loans, which offer more repayment options.

How interest and APR are calculated

Critically, you need to know the difference between interest rates and APR (Annual Percentage Rate). This helps you to understand how much your £200 loan will cost you. Interest rates show what you’ll pay in interest, while APR reveals the real cost by adding fees and charges.

Small loans usually have daily APR calculations instead of yearly ones. Some lenders charge about 0.79% interest each day. This is below the 0.8% limit set by the Financial Conduct Authority. Notwithstanding that, these small numbers add up fast.

For example, if you take a loan of £400 for 4 months with a lender charging 0.79% interest per day, you will pay a total of £624.34. Out of this, £197.48 is for interest. A loan of £200 would cost less, but the calculation is the same.

Small loans can have high representative APRs – sometimes over 1000% for payday loans or between 79.5% and 96.2% for other short-term options. People with lower credit scores might pay higher interest than those with great credit.

How long you can borrow for

On the whole, your £200 loan payment terms range from weeks to months, based on the lender and your situation. On top of that, lenders treat new and returning customers differently.

New borrowers can pay back their loans over 8 months with some lenders. Those who have paid back loans before may have up to 12 months to repay. This makes your payments easier to handle.

What’s more, modern £200 loans often let you pay early without extra costs. These loans charge daily interest, so paying off your balance early helps cut your total interest. The shortest term you can afford comfortably works best.

Lenders use a Continuous Payment Authority (CPA) to take money directly from your bank account on certain dates. This automatic system helps you stay on track with payments and protects your credit score.

Who can apply for a £200 loan?

To begin with, let’s see if you qualify for a quick £200 loan. You can save time and protect your credit score by knowing the qualifying criteria before applying. To explain, let’s get into what lenders usually look for in applications.

Basic eligibility requirements

Most direct lenders keep their requirements simple for £200 loans. You must:

- Be at least 18 years old

- Be a UK resident

- Have a regular income (typically at least £400 monthly from employment, self-employment, or benefits)

- Possess an active UK bank account with a valid debit card

- Have a valid mobile number and email address

These requirements help lenders follow regulations and verify who you are and your financial status. More than that, some lenders might need extra documents during your application, like proof of income or ID.

What if you have bad credit?

In stark comparison to what many think, bad credit doesn’t automatically mean you can’t get a £200 loan. Many lenders actually offer options for people whose credit isn’t perfect.

When looking at applications from people with poor credit, lenders typically:

- Focus more on whether you can repay now rather than past money troubles

- There’s another reason they consider – stable income and regular employment

- Look at how you’ve handled recent payments rather than just your overall score

With this in mind, most FCA-approved lenders will still run some type of credit check as part of responsible lending. So if you see a lender advertising “no credit check” loans, make sure they’re FCA-authorised to avoid scams.

These situations might still get your application rejected:

- Recent CCJs (County Court Judgments)

- Active IVAs (Individual Voluntary Arrangements)

- Current bankruptcy status

How income and expenses affect approval

Of course, your financial situation plays a significant role in getting approved. Lenders must make sure you can pay back loans without further worries.

Lenders will check:

- Your pre-tax annual income, including salary, pensions, regular overtime, commissions, and other income like rental properties

- Monthly expenses such as mortgage or rent payments

- Existing debt obligations including personal loans, credit cards, and hire purchase agreements

This detailed check helps determine if you can manage loan repayments along with your current financial commitments. Having a steady income is good, but if you have a lot of debt, it might make it harder to get approved.

Some lenders have “eligibility checkers.” These tools do a soft credit check to show if you may get approved. This does not harm your credit score. So using these tools before applying can help you find good options without risking your credit score.

Keep in mind that each lender has their own rules beyond these basics. Meeting the basic requirements does not mean you will be approved. The lender will make a decision after reviewing your application.

Comparing your loan options

Presently, a quick £200 loan comes with various options that can help you save money and reduce stress. Let’s look at your choices and how you can make the right decision.

£200 loan from a direct lender vs broker

In this situation, your choice between a direct lender and a broker depends on your priorities.

Direct lenders bring several benefits for a £200 loan. They use their own money and make decisions without other parties. This means faster processing and often lower costs since you won’t pay broker fees. Many direct lenders can send money within 10 minutes after approval.

Generally, credit brokers connect you with different lenders that suit your needs. You get access to several loan offers at once, which could lead to better terms.

The good news is that most FCA-regulated brokers get paid by lenders and don’t charge you anything. It’s worth mentioning that brokers need to share your details with their lender panel, but direct lenders don’t.

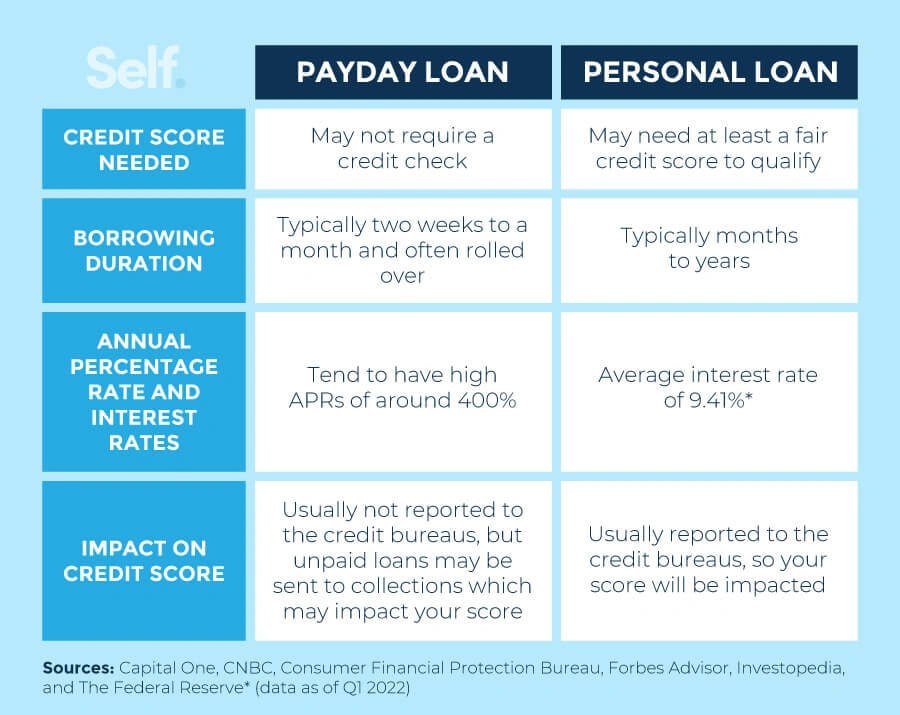

Payday loans vs short-term loans

To clarify, these terms might sound similar, but they’re quite different:

Loans with payday lenders need repayment within a month, usually on your next payday. Short-term loans give you 3 to 12 months to repay, which makes the cost more manageable.

The costs for both options are higher than traditional loans. Payday loans have high interest rates. For a £200 loan for 30 days, the rate can be as high as 1,250%. This means you will owe about £48 in interest.

Importantly, borrower protection rules are simple, meaning you won’t pay more than twice what you borrowed. For example, if you take a £200 loan, the most you will pay is £400. Also, daily interest will not go over 0.8%.

What to check in the loan agreement

Before you accept a £200 loan, take a close look at these vital points:

- APR (Annual Percentage Rate): This shows your yearly cost including interest and standard fees. Lower APRs mean you’ll pay less.

- Repayment terms: Look at your repayment time and payment options.

- Early Repayment Options: Many lenders allow you to pay off your loan early without extra fees. This can save you money since interest usually adds up every day.

- Fees and extra charges: Watch for late payment fees or early repayment charges.

- FCA Regulation: The lender should be registered with the Financial Conduct Authority, helping to keep you safe.

A full picture of these details helps you avoid unexpected issues and pick the best £200 loan for your needs.

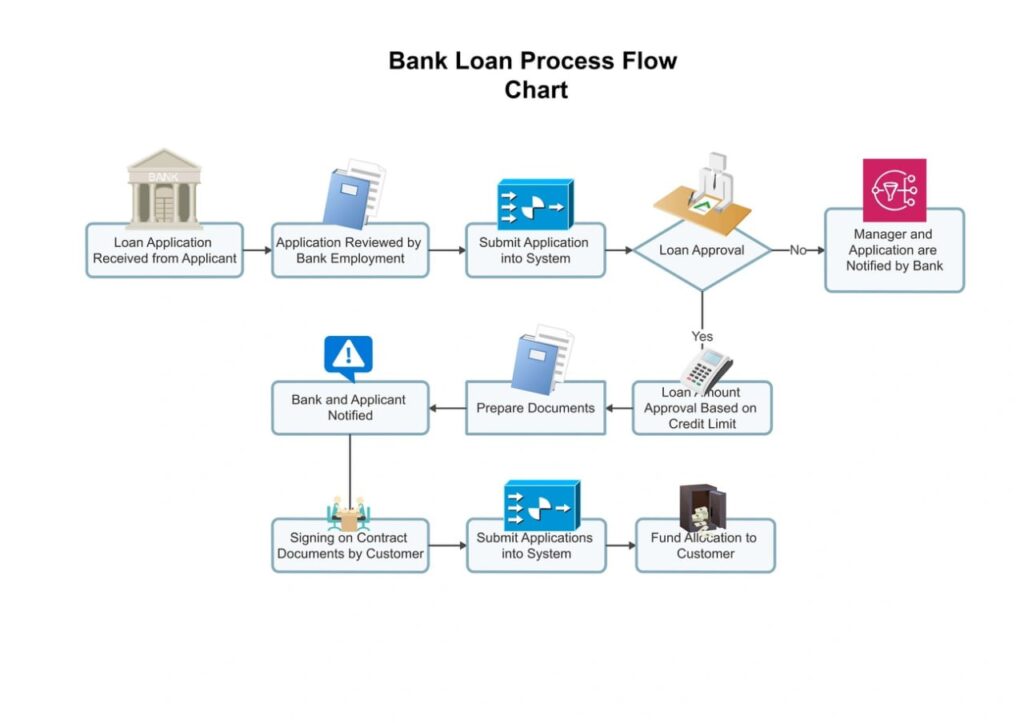

How to apply and get approved quickly

Getting a £200 loan is now much simpler with modern online systems. Here’s how you can get funds quickly when you need them most.

Step-by-step application process

Most importantly, here’s what you need to do to get a £200 loan:

- Choose your loan amount and terms – Pick exactly £200 or adjust as needed (many lenders let you borrow from £50 upward in £10 increments)

- Select repayment frequency – Choose weekly or monthly payments that line up with your payday

- Complete the online application form – Add your personal details, employment information, income, expenses, and banking details

- Submit and wait for assessment – You can fill out most applications in about 5 minutes

- Review and accept offer – Read all terms carefully before accepting

You can do this on any device with good internet—smartphone, tablet, or computer. Once you get approved, a Customer Care agent may call you. This call usually takes less than five minutes to confirm your information.

Using an eligibility checker

Eligibility checkers help you find your chances of approval without affecting your credit score. This helpful tool runs a “soft search” that only shows up on your credit file when you look at it.

You’ll need this simple information to use an eligibility checker:

- Your address history for the last three years

- Monthly take-home pay

- Monthly mortgage or rent payments

Most checks take just 3-4 minutes. You’ll get a percentage score that shows how likely you are to be approved—higher scores mean better chances.

How long approval usually takes

For the most part, you’ll know the decision within minutes after submitting. The time it takes to get your money depends on your lender:

- Ultra-fast: Some lenders send money within 90 seconds of approval

- Very quick: Many transfer funds within 10 minutes (if your bank handles Faster Payments)

- Same-day: Most transfers finish within 24 hours

The quickest way to get your £200 loan is to apply during business hours and check all your details before sending. Keep your phone nearby so lenders can quickly check any extra information they need.

FAQs – Smart ways to repay your loan

Taking care of your quick £200 loan after it is approved is important for your money health. Smart repayment strategies will save you money and protect your credit score.

Setting up automatic payments

Your bank account’s automatic payment feature will give a reliable way to make loan repayments on time.

This helps you avoid late fees and creates a good credit history. Many lenders provide flexible repayment options that line up with your payday. This easy method helps you budget and avoid missed payments.

What happens if you miss a payment?

First thing to remember, a missed payment can trigger late fees ranging from £10-£30 based on your loan agreement. Your credit report will show missed payments after 30 days, and these marks stay visible for seven years. The best approach is to reach out to your lender right away if you expect payment difficulties—most lenders will help find solutions.

Can you extend or refinance the loan?

Indeed, many lenders offer choices to change payment dates when borrowers have problems. Debt consolidation might be a good option if you have good credit and enough money to get a new loan with lower interest rates.

How to avoid falling into debt

A detailed budget should track your income and expenses so you know what you can afford to repay. A credit counsellor from a reliable nonprofit can look at your situation and recommend the best way to move forward.

Conclusion

Without doubt, a £200 loan might look like a small amount, but your choices can substantially affect your finances. This text explains how short-term loans work. It tells you what interest rates you might see and who can get these loans.

Small loans give you quick fixes for surprise expenses without the hassle of bigger loan options. But keep in mind that higher APRs make these loans cost much more than regular financing methods. You should borrow only what you need for the shortest possible time.

Loan applications have become super simple nowadays. Many lenders let you apply online and get your money the same day. Taking time to compare different lenders before you apply will help you get the best deal possible.

What’s more, planning how to pay back is just as important as your first application. Setting up automatic payments that line up with your payday will help you pay on time and protect your credit score. Contact your lender right away if you have trouble making payments. This can help you avoid extra fees and issues with your credit.

A £200 loan can be a handy financial tool if you use it wisely. Think about all your options, know the total cost, and map out your repayment plan before you borrow. This approach will solve your immediate cash needs without causing bigger money problems down the road.

On the positive side, these small loans can help you when you need money. You just have to plan well and pay on time.

Related links