UK Debt Consolidation Loan Guide for 2026

In the previous year, 3.2 million adults across the United Kingdom found themselves turned down for credit, and many of these marks on their records were completely preventable. The stress of needing financial assistance, only to be anxious about how the application process might negatively impact your credit rating, can be overwhelming. Whether you are investigating a debt consolidation loan to manage debt and simplify your finances or in search of new credit options, that fear adds unnecessary pressure.

It’s natural to feel fatigued by the opaque world of broker fees and the anxiety that previous financial errors render you unable to access favorable rates. You deserve a clear pathway to the funds you need without the concern of a diminishing credit score. This is why performing a thoughtful comparison of UK loan brokers is the ideal first action. If you’re aiming to navigate debt and consolidate debt UK without uncertainty, a well-informed comparison allows you to identify viable options before making a commitment.

We are here to assist you in transitioning from financial worry to a state of true empowerment. This guide reveals how to secure optimal rates, including the 5.7% representative APR currently available for larger personal loans and loans for debt consolidation, especially while the Bank of England maintains the base rate at 3.75%.

We will also elucidate how "soft search" technology can safeguard your credit record and how the latest Consumer Duty regulations from the FCA ensure that you receive proper value. From loans for homeowners to short-term solutions and various debt consolidation loan options, here’s how to locate a financial ally who respects your independence and future.

Key Insights

- Understand why brokers offer broader choices compared to direct lenders, who are limited to their own products.

- Conduct a strategic comparison of UK loan brokers by confirming FCA registration and the extent of their lender panel to guarantee maximum transparency.

- Protect your credit rating by prioritizing brokers that employ soft search technology for quotes, ensuring no impact on your credit profile.

- Recognize the right expert for your unique objectives, whether you need a homeowner loan for substantial amounts or a loan for those with bad credit looking for a fresh start.

- Transition from financial tension to empowerment with efficient matching services that concentrate on your present needs rather than judging your prior financial missteps.

- Distinguish when a debt consolidation loan or personal loans for debt consolidation can alleviate your financial burdens and streamline your financial situation.

Table of Contents

- [Navigating the UK Loan Broker Landscape: Broker vs. Direct Lender](Navigating the UK Loan Broker Landscape: Broker vs. Direct Lender)

- [Essential-factors-for-a-uk-loan-broker-comparison-what-to-consider](Essential Factors for a UK Loan Broker Comparison: What to Consider)

- [Evaluating-broker-specialties-from-homeowner-loans-to-bad-credit-solutions](Evaluating Broker Specialties: From Homeowner Loans to Bad Credit Solutions)

- [Utilizing-a-broker-comparison-to-safeguard-your-credit-rating](Utilizing a Broker Comparison to Safeguard Your Credit Rating)

- [Selecting-i-need-cash-your-open-uk-loan-broker](Selecting I Need Cash: Your Open UK Loan Broker)

Navigating the UK Loan Broker Landscape: Broker vs. Direct Lender

Stop guessing which banks might approve your loan request. When you require funding, you fundamentally have two choices.

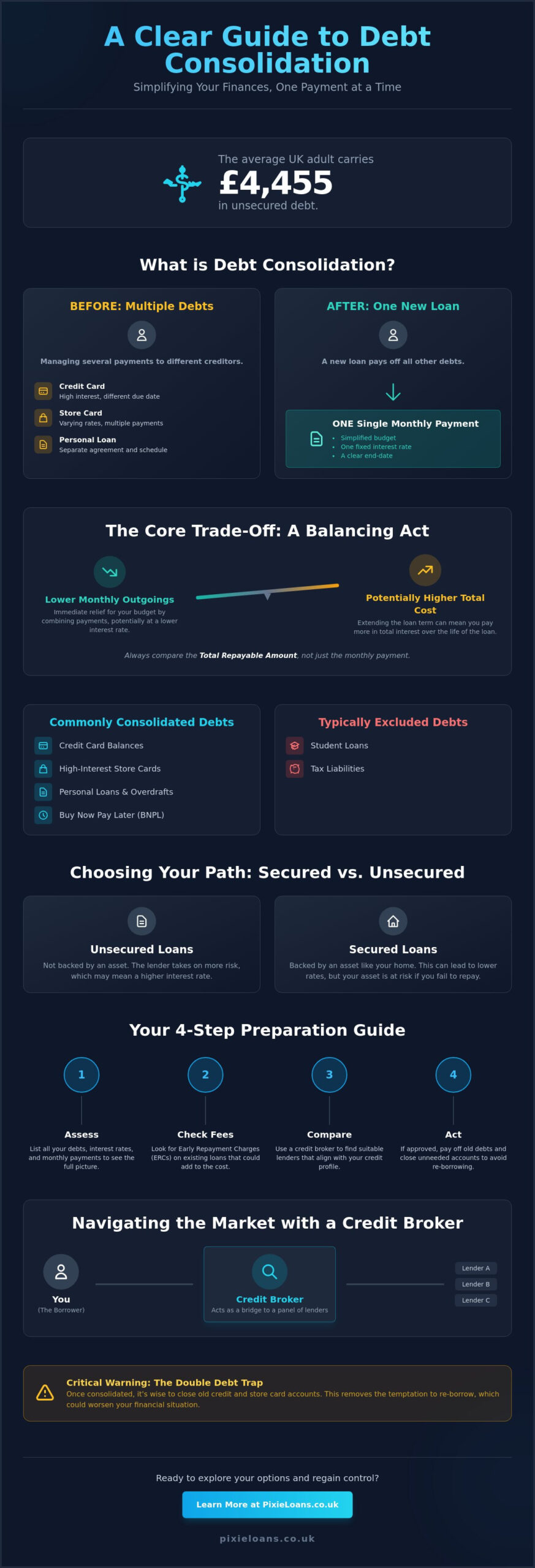

You can approach a direct lender, who only presents their unique products, or you can engage the services of a broker. A broker acts as an authorized intermediary. They do not dispense cash themselves; rather, they present various choices. This choice is crucial if your intention is to manage debt via a debt consolidation loan.

Understanding https://en.wikipedia.org/wiki/Credit_broker helps you to recognize why they are often the preferable ally for your finances. They operate under FCA oversight, serving in your best interest while providing fair value in accordance with the Consumer Duty regulations.

This differentiation is the cornerstone of any effective UK loan broker comparison. While a lender offers the funding, a broker provides the access. Think of it as the "Power of the Panel." Instead of completing ten separate applications for ten different banks, you only need to fill out one form.

Brokers like I Need Cash then navigate an extensive network of providers to discover the best matches for your situation. Most importantly, these matching services are often free of charge for applicants. The broker receives a commission from the lender instead of charging you a fee.

The Importance of Choice in the 2026 Loan Market

High-street banks have considerably tightened their lending standards. Since the Bank of England kept the base rate at 3.75% in April 2026, traditional lenders have become increasingly selective in their approvals.

This shift has paved the way for independent, specialized lenders. Many of these providers do not engage directly with the public and only make their products available through brokers. By utilizing a broker, you can access these "hidden" offers. A larger pool of options naturally leads to more competitive rates for consumers.

The Broker Benefit: Saving Time and Protecting Your Credit Profile

Applying to various lenders separately can be a dangerous tactic. Each direct application typically triggers a "hard search," which leaves a lasting imprint on your credit record. Numerous applications in a short timeframe can portray you as overly desperate for funds and depress your credit rating.

A broker changes the dynamics significantly. They utilize a "soft search" to review your eligibility across numerous lenders simultaneously. This approach does not harm your credit profile. It’s a more secure and quicker way to explore your options, especially if you have complicated financial needs or a poor credit history that requires a lenient lending approach—particularly beneficial when assessing personal loans for debt consolidation.

Essential Factors for a UK Loan Broker Comparison: What to Consider

Avoid settling for the first name that appears in your search results. A comprehensive UK loan broker comparison requires delving into the details to ensure that your financial health is safeguarded. You need a broker that fulfills all requirements, from compliance to operational efficiency.

Start by reviewing the range of products available. An outstanding broker should encompass everything from homeowner loans for significant projects to short-term loans for urgent requirements, and debt consolidation loan options tailored to simplify your finances. Should their selection be too limited, you may miss out on the competitive rates that a broader market exploration offers. Seek a partner who works for you, not one who constrains your choices while offering complete transparency.

The size of the lender panel can be your hidden advantage in securing the optimal deal. A broker with access to over 50 lenders is substantially more likely to discover a match for your individual situation than one with a restricted panel.

Contemporary brokers also employ Open Banking to streamline the borrowing process. This technology allows for quicker, more equitable decisions by securely sharing your transaction history.

It shifts the focus from past errors to your current capacity to manage credit. This promotes personal autonomy, ensuring that the offer you receive is customized to your actual financial situation, aiding you in managing debt based on today’s affordability. If you seek a partner that meets every one of these criteria, you can check your eligibility now without any risk to your credit profile and view your options to consolidate debt UK with confidence.

Confirming FCA Authorization and Safety

Before revealing any personal information, always confirm the broker’s legitimacy by checking the Financial Services Register. This verification is essential to ensure that the broker is genuinely registered and not a fraudulent entity. Authorization is not merely a title; it serves as a protective legal measure.

Under the FCA’s Consumer Duty, which remains a focal point for regulations in 2026, firms must conduct their operations in good faith while providing fair value to every client. This regulation guarantees that your data is handled with the highest standards of security, protecting you from identity theft and ensuring your information is not shared with third parties without your agreement.

Transparency and the "No Upfront Fee" Principle

Exercise caution when dealing with unscrupulous firms that demand payment before presenting a loan offer. Honest UK brokers do not impose upfront fees on applicants. They earn their commission from the lenders only after a successful loan is issued. A genuinely free broker service is one where the applicant incurs no charges to search, compare, or apply—including when evaluating debt consolidation loan quotes.

This commitment to transparency is a vital element of your UK loan broker comparison approach. This model aligns the broker’s incentives with your own; they only prosper when they identify a deal that suits your needs. It is the most effective means to transition from financial fear to a state of complete empowerment.

Evaluating Broker Specialties: From Homeowner Loans to Bad Credit Solutions

In finance, a one-size-fits-all solution is rare. A generic search might lead you to a lender that isn’t quite right for you, underscoring the value of a focused UK loan broker comparison. Different brokers specialize in various market areas, ensuring you aren’t reduced to just another entry on a spreadsheet. If your aim is to unify multiple debts into one payment, numerous brokers specifically focus on personal loans for debt consolidation.

Whether you need an unsecured personal loan ranging from £1,000 to £25,000 or require a prompt solution for an unexpected expense, the right specialist will act as your representative. They comprehend the specific "entry criteria" of their lender network, preventing you from the aggravation of being quickly declined.

Most comparison platforms treat all borrowers similarly, yet the reality involves considerable complexity. Personal loan brokers concentrate on efficiency and attractive APRs, which averaged 6.33% for a £10,000 loan at the start of 2026. Conversely, short-term and payday loan brokers cater to smaller, more urgent needs where urgency is paramount.

By selecting a broker who appreciates these nuances, you are closer to achieving a solution that honors your personal freedom. They don’t just find any loan; they search for one that aligns with your current goals and repayment capabilities. If you want to understand how consolidation loans can simplify your UK finances in 2026, reviewing the latest market trends and representative APRs can help you make a more informed decision before approaching a broker.

Homeowner Loans: Accessing Home Equity

If you’re in search of a larger amount, a homeowner loan often proves to be a more adaptable alternative to a conventional personal loan. These are classified as "second charge" mortgages, allowing you to borrow against the equity in your home without interfering with your primary mortgage. Brokers specializing in this area will assist you in navigating intricate requirements such as property valuations and legal documentation.

Since the loan is secured, you may gain access to more favorable rates or extended repayment terms than with unsecured alternatives. This approach is a strategic way to finance extensive home enhancements or consolidate debts while maintaining manageable monthly payments.

Options for Bad Credit and Minimal Credit Records

A negative credit history shouldn’t permanently block your path to financial assistance. Specialized brokers collaborate with a pool of "friendly" lenders who consider more than just a basic credit score. They prioritize "real-world" lending standards, such as your current income and spending habits, instead of past errors.

This is especially crucial given that 3.2 million adults in the UK faced credit denials lately. For those looking to simplify their financial dealings or consolidate credit card debt with bad credit UK lenders can work with, a well-matched broker can reveal feasible options.

If you possess CCJs or defaults, these brokers can connect you with lenders willing to offer representative APRs typically ranging from 39.9% to 99.9%. For individuals seeking immediate assistance with smaller amounts, payday loan options through a niche broker can provide relief without the judgment often encountered at conventional banks.

Utilizing a Broker Comparison to Safeguard Your Credit Rating

Safeguarding your financial reputation is as important as acquiring a low interest rate. Many individuals incorrectly believe that "shopping around" involves submitting applications to five separate banks in one day. This approach is misguided. Each direct application typically results in a hard search, which is visible to other lenders and can negatively impact your credit score.

An astute UK loan broker comparison serves as a protective mechanism. It enables you to examine the entire market while only undergoing one preliminary check that doesn’t affect your file. This transition takes you from uncertainty to complete control, particularly if you’re seeking to simplify your finances and manage debt predictably.

Brokers are exceptional facilitators because they prioritize your credit health. By utilizing a single form to access a broad panel, you minimize the risk of the "rejection spiral" where too many hard searches make you appear as a high-risk borrower.

A broker provides a secure environment to explore alternatives without the dread of permanent damage. You can assess which lenders are likely to approve you before you commit to a formal application. If you’re ready to explore your options risk-free, begin checking your loan eligibility now.

The Power of the Soft Credit Check

Don’t dread credit inquiries. A soft search is a preliminary assessment that leaves no evidence for other lenders to view. It’s often referred to as a "quotation search" because it’s utilized solely to provide an accurate APR tailored to your current situation.

You can review your personalized terms and evaluate them against various other offers without affecting your ability to borrow in the future. This ethical method of exploring the market guarantees that you only proceed with a hard application when you are confident in the outcome—ideal when comparing debt consolidation loan quotes one alongside the other.

Open Banking: The Standard for Fair Lending in 2026

Approval rates are now based not only on your past but also on your present behavior. An increasing number of modern brokers utilize open banking loans to provide lenders with a clearer overview of your financial situation. This technology allows you to securely share your bank data, demonstrating your affordability even if you have a thin credit profile or prior defaults.

This has revolutionized the process for those with poor credit, as it reveals steady income and responsible spending behaviors that traditional credit scores might overlook. Such technical verification ensures that your application is evaluated based on your actual life circumstances, not just a three-digit figure, making a contemporary UK loan broker comparison the most intelligent borrowing strategy in 2026 and enabling you to manage debt sustainably.

Selecting I Need Cash: Your Open UK Loan Broker

You deserve a financial partner that appreciates your time and your aspirations. After performing a UK loan broker comparison, the choice often hinges on who treats you like an individual.

At I Need Cash, we position ourselves as an understanding intermediary. We recognize that life can present challenges. Past financial missteps shouldn’t permanently mark you with a stigma of denial.

We have designed a platform that transitions you from anxiety to empowerment. Our approach emphasizes speed, utilizing clear, mobile-optimized forms that deliver results in minutes instead of days.

As a digitally driven intermediary, we prioritize openness over traditional procedural norms. We strictly comply with FCA regulations and the Consumer Duty, ensuring that every match we find offers proper value and serves your best interests.

This goes beyond a mere commercial transaction; it involves delivering supportive services. We work for you, leveraging our expansive network to advocate on your behalf rather than acting as a gatekeeper. You can explore your options, reassured that our preliminary search has no effect on your credit profile, thereby lowering entry barriers for everyone. We enable borrowers to consolidate debt in the UK with clarity and confidence, free from judgment.

A Varied Network for Every Financial Journey

Our network operates on a straightforward "Problem-Solution" model. If you encounter a specific financial issue, we deliver a swift solution through our diverse panel of lenders. We provide access to a complete range of credit products, from homeowner loans for significant life events to personal loans for your next achievement, and short-term loans for unexpected setbacks—plus paths for debt consolidation loans and personal loans designed to minimize your payments into one affordable sum.

Even if you are in search of bad credit loans or payday loans, our network includes specialists who prioritize your current affordability rather than merely your history. This diversity grants you the personal agency to select the customized conditions that best suit your life.

Initiate Your Quote Without the Anxiety

Discontinue your worries about hidden fees or complicated terminology. Our search service is entirely free for all applicants. We receive our fees from lenders, ensuring that our focus remains solely on securing you the most favorable match. Our application process is swift and systematic; we request only what is necessary to provide you a fair quote and help you streamline your finances with a clearer strategy.

You can seize control of your financial future today from your phone or laptop. Now is the time to stop feeling alienated by conventional financial institutions and start feeling empowered. Begin your loan quote now and discover how our network can serve you.

Take Control of Your Financial Future Today

You are now equipped with the resources to shift from financial anxiety to complete peace of mind. By conducting a thorough UK loan broker comparison, you ensure that you do not merely accept the first offer; instead, you select the most suitable one. Keep in mind that a credible broker acts as your advocate, utilizing soft search technology to safeguard your credit profile while examining a broad panel of independent lenders within the UK.

You are not alone in this journey, nor should you feel judged for past missteps. Modern lending in 2026 centers around your current capacity to repay and your future prospects.

We are FCA Authorised and Regulated, dedicated to offering a free search service that has no bearing on your credit score. Access a network that values your independence and operates at your required pace. It’s time to leave behind the stress and obtain the funds you need with complete transparency—whether to better manage your debts or to achieve a goal with a carefully aligned debt consolidation loan.

Apply for a customized loan quote today and take the first stride toward a better financial horizon. You’ve got this.

Frequently Asked Questions

Is opting for a UK loan broker a better choice than a direct lender?

A loan broker is frequently the preferred option if you appreciate variety and aim to review several possibilities with just one application. While a direct lender is restricted to their own specific offerings, a broker acts as a mediator to explore an extensive array of providers. This enhances your likelihood of securing a competitive rate customized to your unique financial conditions rather than being constrained by the rigid criteria of a single bank—including when you require a debt consolidation loan.

Do loan brokers impose charges for their services?

Most reputable brokers do not require any upfront fees from applicants for searches or matching services. They generally earn a commission from the lender once your loan is finalized and funded. It’s advisable to steer clear of any company requesting payment before you’ve viewed a loan offer, as transparency is a hallmark of trustworthy and ethical brokerage services, including when you are comparing debt consolidation loan options.

Will employing a loan broker adversely affect my credit rating?

Utilizing a broker will not harm your credit score, provided they use soft search technology for their preliminary eligibility assessments. This form of inquiry is not visible to other lenders and does not leave a lasting record on your financial history. It enables you to carry out a UK loan broker comparison with complete confidence, knowing you can view actual quotes prior to committing to a formal application.

Can I secure a loan through a broker if my credit is significantly poor?

Absolutely, you can discover assistance even if you have a background of CCJs or defaults. Specialized brokers collaborate with a range of lenders who delve deeper than a basic credit score, emphasizing your current income and capacity to repay. They function as a supportive partner, guiding you toward bad credit loans that respect your autonomy and present ability to manage repayments.

How long does it typically take for a broker to secure a loan deal?

Finding a compatible match generally takes just a few minutes due to advanced automated matching systems. After you submit a brief online form, the broker’s technology surveys dozens of lenders in real-time to deliver an immediate outcome. This rapidity is crucial for individuals requiring short-term loans or emergency funds who cannot afford the delays associated with traditional banking—this is also beneficial for expediting decisions on debt consolidation loans.

What details do I need to provide to a loan broker?

You will need to share basic personal information, your address history, and clear documentation of your income and expenditures. Many brokers also employ Open Banking to securely verify your bank transactions almost instantly. This technological approach ensures a quicker and fairer determination, as it offers lenders an unobstructed view of your actual financial behaviors.

Are all UK loan brokers regulated by the FCA?

Every legitimate broker must obtain authorization and regulation from the Financial Conduct Authority (FCA). This regulation acts as a vital consumer protection guarantee, ensuring firms operate in good faith while providing fair value. Always verify a broker’s status using the Financial Services Register before providing any personal information to keep your data safe and protected.

What differentiates a secured loan broker from an unsecured one?

A secured broker focuses on products that are backed by an asset, like homeowner loans, whereas an unsecured broker manages personal loans and payday loans. Secured options usually permit borrowing larger sums since the lender has the assurance of your property. Unsecured brokers facilitate loans based purely on your creditworthiness and current earnings, making them a common choice for smaller, more urgent financial needs. Personal loans for debt consolidation usually fall into the unsecured category, while certain secured homeowner loans can also be utilized for consolidating debt.

How does a broker shield my credit rating while I search for a loan?

Reliable brokers employ a soft credit check to assess your eligibility across multiple lenders without leaving an observable mark on your credit file. This allows you to see potential approvals and indicative APRs without impacting your score. A hard inquiry typically only occurs if you decide to move forward with a formal application to a specific lender.

What should I consider when comparing UK loan brokers?

Always check for FCA authorization on the Financial Services Register, emphasize brokers with extensive and varied lender panels (preferably 50+), and ensure they utilize soft search technology. Favor brokers that support Open Banking for quicker and fairer evaluations, and avoid any that demand upfront payments—their commission should only be drawn from the lender after the loan is successfully funded. Select a broker whose specialty aligns with your requirements (e.g., homeowner loans, bad credit options, short-term needs, or debt consolidation).

What interest rates are available in 2026?

This guide mentions a representative APR of 5.7% available on larger personal loans (including numerous debt consolidation loans), noting that personal loans of £10,000 had average rates of about 6.33% in early 2026. For those with adverse credit, specialized lenders often present representative APRs ranging from 39.9% to 99.9%. Rates can vary based on profile, type of product, and lender criteria, even with the Bank of England’s base rate at 3.75%.

Is a debt consolidation loan always the best option?

Not necessarily—its benefits are greatest when it simplifies repayments and aligns with your current affordability. Whether it reduces overall expenses depends on the new APR, potential fees, and the repayment period in comparison to existing debts. Quotes obtained via a broker’s soft search allow you to compare choices side by side before making a commitment, thereby assessing whether consolidation will enhance your savings or merely reorganize your payments.

Should I consolidate debts using an unsecured personal loan or a secured homeowner loan?

Unsecured personal loans (often ranging from £1,000 to £25,000) are generally quicker to obtain and do not necessitate collateral, making them common for consolidating moderate debts. Homeowner loans are secondary mortgages secured against your property’s equity; they can offer larger borrowing amounts, potentially lower rates, or extended repayment terms—but because they are secured by your home, you must be comfortable with the added risk and additional procedures, such as valuations and legal requirements. For those specifically looking to consolidate credit card debt with bad credit in the UK, unsecured personal loans through a specialist broker are often the most accessible starting point.

APPLY TODAY

—————————

Related links

How to Find Best Car Finance Options in the UK: A Money-Saving Guide

The Ultimate Guide on How to Secure a Car Loan

How to Find the Best Car Loan Deals Online: A Smart Buyer’s Guide

What are the types of Car Loans

Choosing Your Perfect Car: A Smart Guide to Best Loans for Cars