Short Term Loans: A Transparent Guide to Fast Borrowing in the UK

Did you know that one in four UK consumers planning a personal loan in 2026 will use it to get by? They may also use it to cover an unexpected money shortfall.

It’s a stressful position, especially when an urgent bill arrives and your monthly budget is already fully spent. You likely want a fast solution that stays clear.

Yet the short-term loan market can feel cluttered. It often uses complex jargon. Many people are unsure about the difference between brokers and direct lenders.

We’ve developed this comprehensive guide to help you move forward with confidence. It offers a professional view on how to access funds responsibly. It also keeps the total borrowing cost in clear focus.

If you want to understand current FCA price caps, or choose a repayment plan that fits you, this article can help. We will explain how fast borrowing works.

We will explain why modern affordability checks matter. We will show you how to find a practical short-term solution.

Key Takeaways

- Learn how short term loans can help cover emergency costs. They offer a regulated bridge and follow strict FCA consumer protections.

- Learn why focusing on the total amount you repay shows borrowing costs more clearly than the APR alone.

- Discover how a credit broker helps you compare many lenders with one simple application.

- Explore why soft searches matter in applications. They help protect your credit file during the quote stage.

- Identify the best path for your needs. Compare short-term options with unsecured loans or debt consolidation loans.

Table of Contents

- What are Short Term Loans and How Do They Function in the UK?

- The Mechanics of Repayment: APR vs Total Cost of Borrowing

- Broker vs Direct Lender: Finding Your Best Fit

- Requirements and the Application Process: A Step-by-Step Guide

- Responsible Borrowing: Making Short Term Loans Work for You

What are Short Term Loans and how do they work in the UK?

Short-term loans are a focused financial tool for times when an unexpected expense exceeds your monthly cash flow. Unlike traditional bank loans with multi-year commitments, these products are meant to be paid off fast. They are often settled within a few months.

To understand short-term loans today, think of them as a temporary bridge. They are not a permanent part of your finances.

If you find yourself returning to a "favourite" lender out of habit, you might be missing out on more appropriate options. The UK lending market is competitive and diverse. A provider that suited your needs last year may not be the best choice now. Our role is to be a practical guide, helping you find short term loans that fit your financial profile when you need them most.

The Core Purpose of Short Term Borrowing

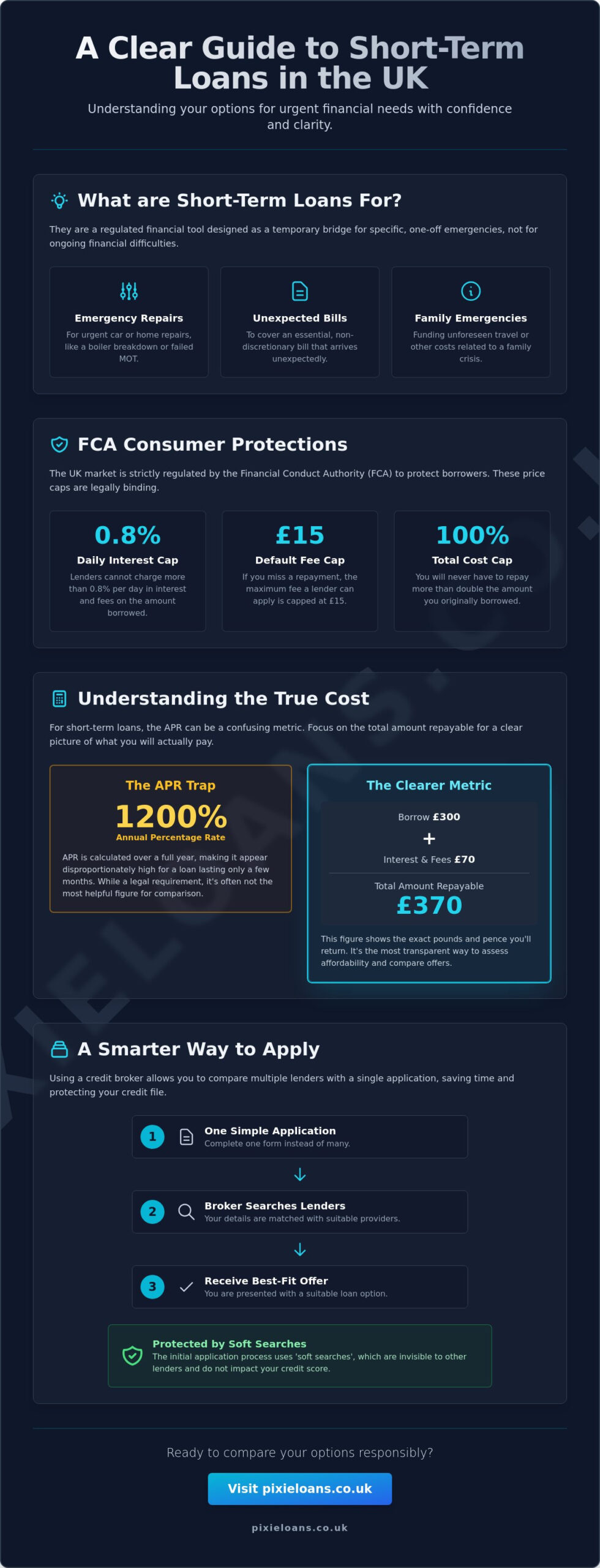

These financial products are specifically engineered for one-off emergencies. If your car fails its MOT or your boiler breaks down in winter, a short-term cash boost can fix it fast. They’re effective for:

- Emergency home or vehicle repairs.

- Urgent, non-discretionary bills.

- Unforeseen travel costs for family emergencies.

Recognising that these loans are not a good fix for ongoing money troubles is vital. If you’re struggling to meet basic living costs every month, taking on additional credit could worsen the situation. In such cases, seeking free debt advice is always the more responsible path.

Understanding the UK Regulatory Landscape

The UK market is one of the most strictly regulated in the world. The Financial Conduct Authority (FCA) regulates it. These regulations aim to prevent borrowers from falling into debt spirals.

For instance, the FCA has implemented a strict price cap on high-cost short-term credit. Lenders can charge up to 0.8% of the amount borrowed per day in interest, and they can charge default fees up to £15. Most importantly, you will never have to repay more than 100% of the original loan amount.

Transparency is a legal requirement for both lenders and brokers. If a firm acts as an intermediary, it must clearly state its role and explain how it receives remuneration. This ensures you have full information before you commit to any agreement.

By requiring strict affordability checks, the regulator gives credit only to people who can repay it. This methodical approach to short term loans ensures that the financial journey remains predictable and manageable for the consumer.

The Mechanics of Repayment: APR vs Total Cost of Borrowing

When you compare different financial products, the Annual Percentage Rate (APR) is usually the first figure you see. However, for short term loans, the APR can be a misleading metric. Because APR shows the cost of credit over a full year, using it for a three- or six-month loan can seem too high. While it is still required by law for comparison, it may not match what you pay over a few months.

Focusing on the total amount repayable is a more transparent way to evaluate affordability. This figure shows the total you will repay. It includes the principal and all interest charges.

If you want responsible borrowing advice, understanding the "cost per £100 borrowed" can be clearer than a percentage. By checking the total cost, you can decide if the loan’s convenience is worth the expense for your emergency.

Decoding Loan Computation

Loan computation is the process of calculating interest and principal repayments over time. Lenders typically determine interest rates by evaluating your credit risk and the specific amount you wish to borrow.

If you choose a longer repayment term, your monthly instalments will be smaller. However, you will pay more total interest over time.

Conversely, a shorter term means higher monthly outgoings but a lower overall cost. A balance exists between what you can afford each month and how much you’re willing to pay for the credit in total.

Fixed vs Variable Repayment Structures

Most short term loans in the UK utilise fixed repayment structures. This means your monthly payment stays the same during the agreement. It lets you plan your household budget more accurately.

If your circumstances improve during the term, many lenders allow for early repayment. This is a major advantage.

It can cut the total interest you owe. It does this by shortening how long the balance stays unpaid.

Clear repayment dates are essential. If you match them to your payday, you can avoid late fees. You can also keep a healthy credit score.

Before you sign an agreement, it makes sense to review your options with a broker. This helps you see how different repayment terms affect your total cost. This methodical approach ensures you don’t overstretch your finances while addressing your immediate needs.

Broker vs Direct Lender: Finding Your Best Fit

Choosing between a broker and a direct lender is a pivotal decision that shapes your borrowing experience. While a direct lender provides the funds and manages your repayment, a credit broker helps connect you to lenders. Rather than contacting companies one by one, a broker uses one application to search many lenders.

This step-by-step approach helps you find short term loans that match your financial profile. It saves you time and effort by avoiding manual comparisons.

A common misconception in the UK market is that using a broker adds an unnecessary layer of cost. In reality, reputable brokers for short term loans do not charge the applicant a fee for their matching services.

The lenders themselves typically remunerate them. This means you gain the advantage of a wider market search without increasing your total cost of borrowing. If you have a complex credit history, this broad search can help, as it links you with specialist providers.

These providers work with many financial backgrounds, not narrow or rigid criteria.

The Broker Advantage

The primary benefit of a broker is the efficiency provided by modern financial technology. When you send your details through an FCA-authorised broker like Pixie Loans, our system checks them right away.

It compares them with the criteria used by many lenders. This significantly reduces the risk that a single institution’s specific internal policies will reject it.

By matching you with a suitable product from the outset, the process becomes more predictable. It ensures that the financial bridge you’re seeking is both available and structured to meet your immediate needs.

Direct Lenders: What You Need to Know

Direct lenders provide the capital and are your point of contact throughout the life of the loan. However, applying to a single direct lender can be restrictive. If your profile doesn’t perfectly align with their "ideal" borrower model, you may face an immediate rejection. This can be frustrating when you’re dealing with an emergency.

While browsing the UK market, always check that a lender is legitimate.

Verify their status on the Financial Services Register. A legitimate provider will be clear about their FCA authorisation. They will not ask for upfront fees before processing your application.

If you want more choice, you can explore several options before you commit. The broker model is more transparent than using one direct lender. It helps you see more of the market, so you can find a repayment plan that fits your household budget.

Requirements and the Application Process: A Step-by-Step Guide

If you’re ready to apply for short term loans, learn the basic criteria rules first. This helps you get approved.

Most UK providers require you to live in the United Kingdom. You must be 18 or older and have a regular income.

This income does not always need to come from full-time work. Many lenders accept part-time work or certain benefits. For those running businesses in the hospitality, retail, or mobile services, you can learn more about specialised payment processing and card machines to help manage your revenue, ensuring monthly repayments stay affordable within your budget.

One of the most significant advantages of using a modern broker is the implementation of "soft search" technology. Unlike a hard credit check, a soft search lets a broker assess your details with many lenders.

It does not leave a visible mark on your credit report. This is a critical protection for your credit score.

If you were to apply to several direct lenders individually, each one might perform a hard search. Multiple hard searches in a short time can lower your credit score. This can make it harder to get credit later. By using a broker, you maintain the integrity of your credit file whilst exploring your options.

Preparing for Your Application

Before you begin, it’s efficient to organise your personal and financial details to ensure the process moves quickly. You’ll typically need to provide:

- Your address history for the last three years.

- Provide the bank account details for the account where your income is paid.

- A transparent breakdown of your monthly income and essential expenditure.

Accuracy is vital. If your figures do not match your bank statements, it may cause delays or lead to rejection. Lenders value honesty regarding your existing financial obligations, as it allows them to perform a responsible affordability assessment.

The Path from Quote to Payout

Once you’ve received a quote based on a soft search, the final stage involves a formal application with your chosen lender. At this point, the lender will perform a hard credit check to finalise the agreement.

Many modern providers now use open banking technology to verify your income and spending habits securely and instantly. This provides a real-time view of your financial health, which is often more useful than a static credit score. When you need quick loans in the UK, a lender typically transfers funds via Faster Payments once they finalise their checks.

Taking a methodical approach to your application helps ensure a smooth and predictable journey. If you want to understand exactly how to apply for payday loans safely before you commit, our step-by-step guide walks you through the full process. If you’re ready to see which short term loans fit your profile, start your application with us today. You’ll get a clear quote, and it won’t affect your credit score.

Responsible Borrowing: Making Short Term Loans Work for You

Taking a careful approach to credit helps keep short-term loans useful, not stressful. Before you sign an agreement, you must check if this financial product fits your current needs.

If you require a larger sum for a longer duration, unsecured loans might offer a more cost-effective structure. Similarly, if your main goal is to combine several payments, a debt consolidation loan may be a better long-term choice.

Pixie Loans acts as a responsible bridge, linking you to many options and giving clear details to help you decide. We believe that transparency is the foundation of trust. By showing you clear details on total costs and repayment schedules, we help you assess your situation before applying. This makes logic and planning guide the borrowing process rather than urgency alone.

Assessing Affordability and Suitability

The most practical way to start your evaluation is to use a UK loan calculator.

It can help you estimate your possible monthly payments. This tool helps you visualise how a new repayment fits into your existing household budget.

- If the estimated instalment is hard to afford, the loan may not be right for you.

- If you cannot pay for essentials, do not take the loan.

Essentials include rent, utilities, and groceries. When you feel overwhelmed by debt, or you borrow to cover basic living costs, get free financial advice. Seek support from StepChange or MoneyHelper. This is often the most responsible next step.

Managing Your Loan Effectively

Once your loan is active, setting up a Direct Debit is the simplest way to ensure your repayments are made on time every month. This automated approach prevents late payment penalties and helps you maintain a positive credit history.

If your financial circumstances change unexpectedly during the loan term, you should contact your lender immediately. Most FCA-regulated providers have established protocols to support customers facing temporary difficulties. By managing your short term loans with discipline and clear communication, you can handle an emergency.

You also show reliable credit habits that may help with future financial applications.

Moving Forward with Financial Clarity

Managing an unexpected expense requires a methodical approach to evaluating your options. By looking at the total cost of borrowing, not just the percentages, you are making a better choice.

By using soft searches, you are protecting your credit health.

You are also meeting an immediate need. Remember that short term loans work best as a short bridge for one-off emergencies. They are not a long-term financial fix.

If you’re ready to explore your options, Pixie Loans is here to act as your pragmatic facilitator. As an FCA-authorised credit broker, we offer access to many independent UK lenders. You apply once using our simple, efficient application.

Our process is entirely transparent, and we don’t charge any broker fees for our matching services. This ensures you can compare manageable repayment structures without adding unnecessary costs to your journey.

Take the time to assess your affordability and select a path that fits your household budget. Find the right short-term loan for your needs with Pixie Loans and regain control over your finances with confidence. With the right information and a structured plan, you can navigate your current challenge and move forward with peace of mind.

Frequently Asked Questions

How quickly can I receive a short-term loan in the UK?

You could receive your funds on the same day we approve your application. Most UK lenders use the Faster Payments system. It enables near-instant transfers after both parties sign the final contract.

Modern digital lending is often fast. It can go from quote to payout in a few hours. Some applications may take longer if the process requires extra checks. This is after final approval.

Can I get a short-term loan if I have a bad credit history?

Yes, having a less than perfect credit history does not automatically disqualify you from accessing short term loans. Many lenders on our panel offer bad credit options.

They focus on your current affordability and steady income. They do not focus on past mistakes. If you can show that monthly repayments fit your budget, you may still find a suitable lender through our matching service.

Is it better to use a broker or a direct lender for a short-term loan?

Using a broker is often more efficient if you want more choice. It also lets you compare several options with one application. A broker acts as a practical helper and checks many lenders to find a match for your profile. Applying to one lender limits your options and may lead to rejection if you miss their strict criteria.

Will applying for a short-term loan affect my credit score?

The initial quote stage with a broker involves a soft search, which has no impact on your credit score. However, if you choose a specific lender, they will do a hard credit check for the final review. This hard check is visible to other lenders. If you manage repayments well and pay the balance on time, this positive behaviour can help strengthen your credit profile.

What is the maximum amount I can borrow with a short-term loan?

The amount you can borrow depends on a lender’s assessment of your affordability and your specific financial needs. Most UK short-term loans cover smaller, emergency expenses. During the application process, the lender will review your income and spending.

This helps ensure the requested amount does not strain your monthly budget. It also keeps the loan responsible and manageable for your situation.

What happens if I cannot make my loan repayment on time?

If you cannot make a repayment, contact your lender as soon as possible. Discuss your situation with them. Under FCA regulations, lenders must cap default fees for high-cost credit at £15 maximum. Late payments can hurt your credit score.

However, lenders must treat customers fairly. They may offer a revised repayment plan. This can help you manage the debt during temporary difficulties.

Are there any hidden fees when using a credit broker like Pixie Loans?

No, there are no hidden fees or upfront charges for using the matching services provided by Pixie Loans. We are a transparent credit broker. We receive our payment from the lenders on our panel, not from applicants. This lets you access many financial products and compare lenders without raising your total borrowing costs.

Can I repay my short-term loan earlier than agreed?

You have the right to repay your loan early at any point during the agreement. Doing this is often a smart financial move.

It can greatly reduce the total interest you pay. Because interest is usually calculated daily, paying your balance early can lower your interest costs. You only pay interest for the days you used the funds. Always check your specific agreement for any early settlement terms.

Related links

Top UK Direct Lenders for Same Day Cash Loans

UK 12 months loans – how much you can borrow

How to get 200 pound loan approved