Planning Your Dream Day: A Guide to Wedding Loans with Poor Credit in 2026

Planning Your Dream Day in 2026

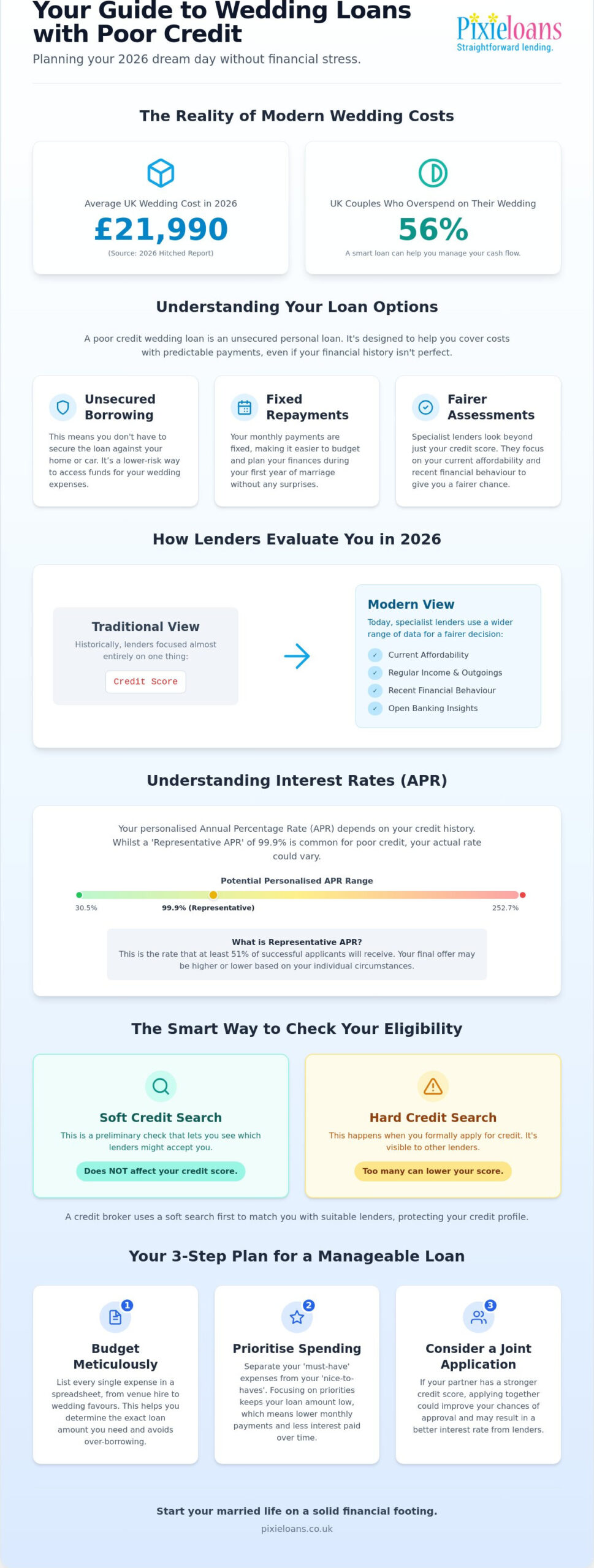

What if your credit history didn’t have to stop your dream wedding? As noted in a recent 2026 Hitched report, 56% of UK couples overspend, but you can plan smarter. If you’re worried about rejection, a wedding loan with poor credit provides a path forward. We’ll help you find affordable repayments whilst protecting your score. This guide explains the broker vs lender difference. Experts at MoneyHelper suggest that early planning is key. Start your journey with confidence using data from GOV.UK.

Key Takeaways

- Learn how unsecured personal loans offer fixed repayments to help you organise your wedding budget with confidence.

- Understand the specific UK eligibility requirements, such as residency and income, to improve your chances of a successful application.

- Discover how to prioritise your ‘must-have’ expenses to secure a wedding loan with poor credit that remains affordable.

- See how a credit broker can efficiently match you with specialist lenders who are most likely to accept your unique profile.

Understanding Wedding Loans with Poor Credit in the UK

A wedding loan with poor credit is an unsecured personal loan tailored for those with less-than-perfect financial histories. With the average UK wedding cost in 2026 reaching £21,990, external funding has become a common choice amongst modern couples looking to manage their cash flow. Whilst interest rates may be higher than standard bank products, these loans provide fixed repayments to help you organise your monthly budget without surprises. If you only need a small amount to secure a photographer or florist, short term loans can serve as a flexible tool for smaller deposits.

Unsecured vs Secured Wedding Loans

Unsecured loans are a form of unsecured debt, which means you don’t have to put your home or car at risk as collateral. This is a common concern for borrowers with a poor credit history who want to avoid the risks associated with secured lending. Unsecured options are often the favourite for wedding expenses like catering, flowers, or dresses because they provide quick access to funds. Since no asset valuation is required, you can often receive a decision much faster, helping you book your dream venue before the peak season.

Why Your Credit Score Isn’t the Only Factor

Specialist lenders on our panel look at your current affordability and financial behaviour rather than just focusing on past mistakes. They use modern criteria to ensure that any loan offered is suitable for your current income and outgoings. This approach provides a fairer chance for couples who have worked hard to improve their financial situation recently. For a deeper look at your borrowing options, you can read our comprehensive 2026 guide to bad credit loans. By evaluating your total financial picture, these lenders help you start your married life on a solid footing.

Evaluating Your Eligibility and Interest Rates

To qualify for a wedding loan with poor credit in the UK, you typically need to be over 18, a UK resident, and have a regular income. Lenders focus heavily on affordability to ensure you can manage the debt alongside your daily costs. If you’re on certain benefits, you might even qualify for a Budgeting Loan, which is an interest-free alternative for essential costs like clothing or household items.

When looking at rates, you’ll see a “Representative APR”. This is the rate at least 51% of successful applicants receive. For those with poor credit, this is often 99.9%. However, your personalised rate could range from 30.5% to 252.7% based on your specific history. To understand how these numbers affect your wallet, it’s a good idea to use a loan calculator to see your potential monthly repayments before you commit.

Lending trends in 2026 have shifted towards “open banking”. This technology lets lenders look at your real-time spending habits rather than just a static credit score. It provides a more accurate picture of your financial health, often helping those who have been rejected by traditional banks. This modern approach ensures that lenders base their decisions on your current behaviour rather than mistakes from years ago.

The Role of Soft Credit Searches

A soft credit search is a preliminary check that doesn’t affect your credit score. It’s a vital tool because it lets you see which lenders might accept you without leaving a visible footprint. This prevents a “rejection spiral” where multiple hard searches in a short time make your credit profile look weaker. You can safely check your options through our online application form to find a suitable match for your needs.

Understanding Unsecured Loans for Bad Credit

Unsecured loans are a type of borrowing that allows you to access funds without putting your car or home at risk as collateral. For more details on how these work, read our unsecured loans for bad credit UK practical guide.

Practical Steps to Organise Your Wedding Budget

Start by listing every expense, from the photographer’s deposit to the centrepieces. Since 56% of newlyweds admit to overspending, a detailed spreadsheet is essential for your planning. This prevents hidden costs from surprising you later in the process. Write down confirmed quotes for your dress, catering, and venue. This helps you determine the exact amount you need when applying for a wedding loan with poor credit.

Prioritise ‘must-have’ expenses over ‘nice-to-have’ features to keep your costs down. Focus on the venue and legal fees first. If the budget is tight, cut back on elaborate floral displays or expensive favours. Keeping your loan amount low reduces your monthly interest costs. It’s better to have a smaller, manageable loan than one that causes stress during your first year of marriage.

Evaluate if a joint application with your partner is a practical strategy. If your partner has a stronger credit score, applying together might improve your chances of approval. Lenders often look at the combined income and history of both applicants. This can lead to better terms amongst specialist providers. It’s a sensible way to approach borrowing for your wedding whilst protecting your financial future.

Borrowing only what is necessary is the most responsible path. The average wedding debt is £3,958, so try to stay near this figure to ensure repayments remain affordable. Financial experts often suggest that borrowing within your means is the key to a stress-free start to married life. For more context, research loans for bad credit to see how different lenders compare.

How to Build a Repayment Plan

Set up direct debits for your repayments immediately to help repair your credit score. Consider the ‘buffer’ method by borrowing slightly more than your initial quotes to cover unexpected 2026 price rises. Consistent behaviour shows future lenders that you’re a reliable borrower. It also gives you peace of mind, knowing your obligations are handled automatically every month without you having to remember each date.

Alternatives to Traditional Loans

Check if you qualify for a 0% purchase credit card for smaller items like accessories. Using personal savings to reduce the loan amount is also a smart move. The less you borrow, the less interest you’ll pay over the life of the loan. You can check your eligibility today through our simple online platform to find a solution that fits your specific needs.

Why a Credit Broker is a Sensible Choice for Your Big Day

Using a credit broker is often the most efficient way to secure a wedding loan with poor credit. Unlike direct lenders who only check their own criteria, a broker scans a whole panel of specialist lenders simultaneously. This transparency ensures you see a range of options tailored to your specific financial background. It acts as a bridge, connecting you to the provider most likely to say yes. By using this model, you avoid the frustration of multiple individual applications that could harm your credit file.

Wedding planning is time-consuming, with many couples admitting to budget overruns. A broker saves you hours of manual research and comparison. Instead of filling out dozens of forms, you provide your details once. This efficiency allows you to focus on the more enjoyable aspects of your big day, like choosing a venue or tasting cakes. If you have an urgent vendor payment due soon, it’s wise to check your emergency loan eligibility to see how quickly you can secure funds.

The Pixie Loans Matching Process

Our application form is designed to be simple and takes only a few minutes to complete. We use modern technology to match your profile with lenders who understand poor credit histories. It’s important to remember that Pixie Loans is a broker, not a direct lender. We don’t provide financial advice, but we do facilitate a clear path to the financial products you need. This process is transparent and designed to protect your credit score through soft search technology.

Final Thoughts on Borrowing Responsibly

Starting your married life on a solid financial footing is the best gift you can give yourselves. Whilst a wedding loan with poor credit provides the necessary funds for your dream day, managing it well is what matters most. Responsible borrowing today builds a better credit score for your future together. By making every repayment on time, you’re not just paying for a party; you’re investing in your financial reputation. We’re here to help you find a manageable solution that lets you celebrate without long-term worry.

Take Control of Your Finances and Plan Your Dream Wedding

Securing a wedding loan with poor credit is a practical way to manage your 2026 celebration costs. As a 2026 Forbes Advisor article notes, specialist lenders provide vital lifelines for those with lower scores. As an FCA regulated broker, we use soft search technology to protect your credit profile whilst finding suitable matches. Apply for a Wedding Loan through Pixie Loans Today. For additional budgeting support, visit MoneyHelper. We’re here to help you start your married life on a solid financial footing.

Frequently Asked Questions

Can I get a wedding loan with very bad credit in the UK?

Yes, you can. “Lenders now prioritise current affordability over historical data,” states a 2026 Financial Times report. This means your current behaviour is what matters most to specialist providers. If you can prove a stable income and manageable outgoings, a wedding loan with poor credit is a realistic option for your 2026 ceremony. It’s about your ability to pay today, not mistakes made years ago.

How much can I borrow for a wedding if I have poor credit?

You can typically borrow between £1,000 and £5,000. According to a 2026 MoneyFacts article, specialist providers cap these amounts to ensure monthly repayments stay within a safe limit. This range covers many venue deposits or essential catering costs. By borrowing only what you need, you ensure your debt remains manageable. This helps you avoid the financial stress that 56% of newlyweds face after their big day.

Will applying for a wedding loan through a broker hurt my credit score?

No, it won’t. “Soft searches are essential for credit health,” notes a 2026 guide from the FCA. These initial checks allow you to see your eligibility without leaving a visible mark on your file. A hard search only happens when you accept a specific loan offer. This technology allows you to compare different lenders whilst keeping your credit score perfectly safe from unnecessary harm.

Are there no-guarantor wedding loans available for those with poor credit?

Yes, no-guarantor options are widely available. A recent 2026 study by the University of Bristol highlights that “unsecured, no-guarantor loans are becoming the standard for modern couples.” You can apply for a wedding loan with poor credit based solely on your own income and affordability. This provides you with financial independence and privacy. You don’t have to rely on family members to co-sign your application to secure the funds.

What happens if I cannot afford my wedding loan repayments after the big day?

You should contact your lender immediately to discuss your options. “Proactive communication prevents debt spirals,” claims a 2026 article by StepChange. Lenders are required to treat you fairly and may offer a temporary payment freeze or a new repayment plan. Taking early action helps protect your credit score from defaults. It ensures that you manage your finances responsibly as you begin your new life as a married couple.