Small Personal Loans UK: A Practical 2026 Guide to Minor Borrowing

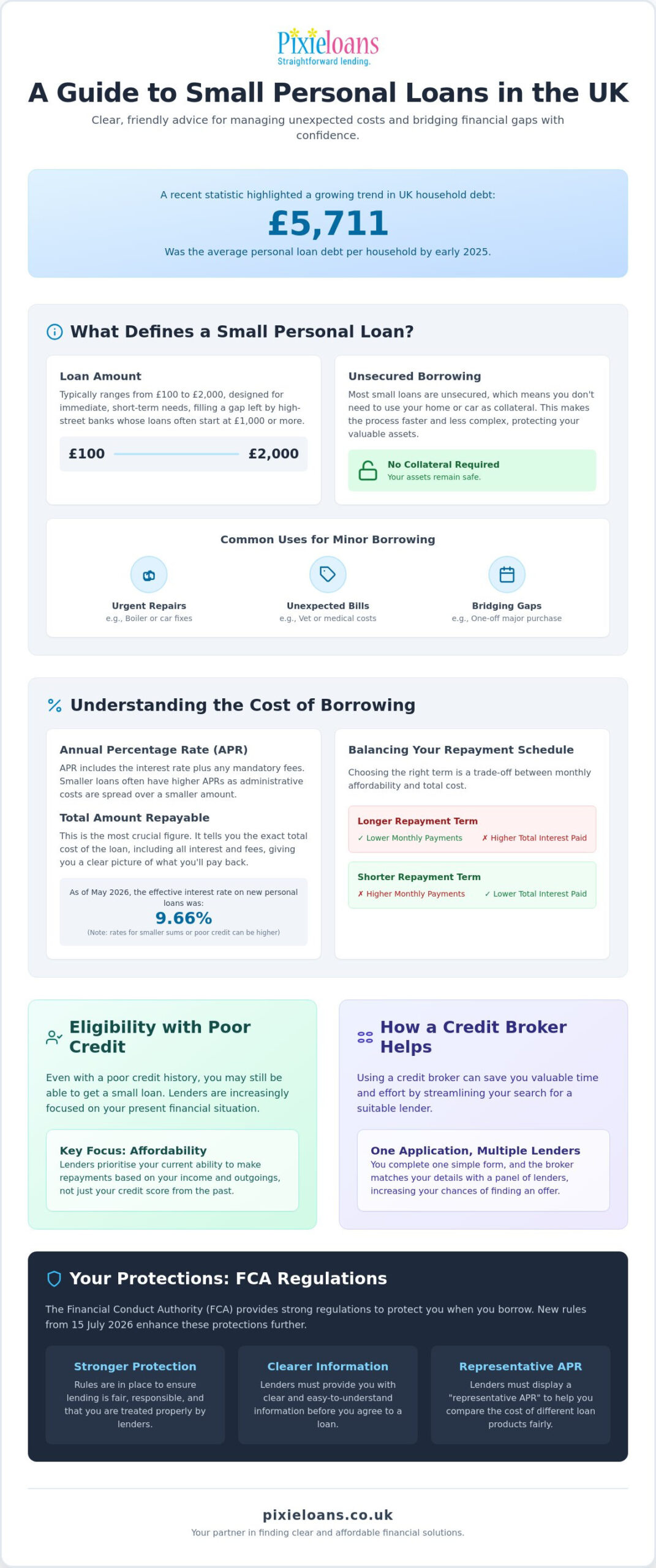

Did you know that the average personal loan debt per UK household reached a record high of £5,711 by early 2025? If you’re looking for small personal loans uk, you’re amongst a growing number of people seeking a tactical way to manage an unexpected bill or an urgent repair. It’s natural to feel some anxiety about high interest rates or how a new application might affect your credit score. You deserve clear, honest guidance whilst you look for a safe way to bridge your financial gaps.

We agree that finding a loan should be a transparent process that leaves you feeling secure. This guide promises to help you find an affordable small loan by explaining the latest 2026 costs and repayment terms clearly. We’ll look at how a credit broker matches you with suitable lenders, discuss the FCA regulations that began on 15 July 2026, and provide a simple path to a successful application. You can find more data on current lending trends via the Office for National Statistics.

Key Takeaways

- Learn what qualifies as minor borrowing in the UK and why these unsecured options mean you won’t need to use your home as collateral.

- Understand how the Annual Percentage Rate (APR) affects your monthly repayments to help you choose the most affordable option for your budget.

- Discover how to navigate small personal loans uk even with a poor credit history by focusing on your current ability to repay.

- Explore how a credit broker can efficiently match you with multiple lenders using one simple application to save you valuable time.

- Gain clarity on the latest 2026 FCA regulations that provide you with stronger protections and clearer information when borrowing small amounts.

What defines a small personal loan in the UK?

A small personal loan typically ranges from £100 to £2,000 in the UK market. Unlike traditional bank loans that often start at £1,000 or £3,000, these smaller sums are designed for immediate, short-term needs like car repairs or boiler fixes. Because they’re unsecured, you don’t need to use your home or car as collateral. It’s a pragmatic way to handle minor financial hiccups without risking your assets. Before you apply, it’s wise to check your emergency loans eligibility to understand what options might be available for your specific situation.

Common uses for minor borrowing

Small loans act as a financial bridge during unexpected life events. For instance, if your fridge stops working or your car needs a quick repair to keep you on the road, a small sum can help. Consider a specific example: an emergency vet bill of £300 that you can’t cover from your monthly budget. These loans provide a structured repayment plan for these one-off costs. Understanding the history of small loans in the UK shows how these products evolved to meet this exact consumer demand.

Unsecured vs secured small loans

Most small personal loans uk are unsecured. This means the lender decides whether to offer you money based on your creditworthiness and income rather than an asset like your house. If you have a lower credit score, you might look for unsecured loans for bad credit uk. Secured loans are rare for small amounts because the legal costs of charging an asset often outweigh the loan’s value. Unsecured options are generally faster and less complex for minor borrowing.

Micro-loans: Filling the high-street gap

Many large high-street banks have moved away from micro-lending, often setting their minimum loan amount at £1,000 or even £3,000. This leaves a significant gap if you only need small personal loans uk for £200 or £500. Specialist lenders and brokers now fill this space, using advanced data to assess affordability quickly. By focusing on these smaller amounts, you avoid borrowing more than you actually need whilst keeping your interest costs lower and your repayment period shorter. This is a sensible approach to maintaining your overall financial health.

Understanding the cost of borrowing small amounts

Borrowing money always comes with a cost. For small personal loans uk, this cost is mainly shown as the Annual Percentage Rate (APR). This figure isn’t just the interest rate; it also includes any mandatory fees the lender charges. You might notice that smaller loans often have higher APRs than large bank loans. This happens because the administrative costs are spread over a shorter term and a smaller amount of money. It’s a standard feature of the minor borrowing market.

Instead of just looking at the monthly payment, you should always check the “total amount repayable”. This tells you exactly how much the loan will cost you in the end. To stay organised, you can use a loan calculator to see how different amounts fit your budget. It’s a great way to ensure your plan is realistic and manageable. For more impartial help, you can consult the Citizens Advice guide to borrowing.

How interest is calculated

Most lenders in this market use fixed interest rates. This means your payments stay the same every month, making it easier to plan your spending. You won’t have to worry about rates rising suddenly. “According to the FCA, lenders must show a representative APR to help you compare options fairly.” This rule ensures transparency across the market. As of May 2026, the effective interest rate on new personal loans was 9.66%, though rates for smaller sums or poor credit can be higher.

Managing your repayment schedule

Choosing the right repayment term is a balancing act. If you pick a longer term, your monthly payments will be lower, but you’ll pay more interest overall. A shorter term saves you money on interest but requires higher monthly instalments. For example, a 200 loan is usually repaid over just a few months. If you feel ready to explore your options, you can start your request online today.

Eligibility criteria for small loans with poor credit

To qualify for small personal loans uk, you must meet a few basic requirements. Lenders generally ask that you’re at least 18 years old, a UK resident, and have a regular income. Some specialist lenders might require a minimum annual income of around £18,000 to ensure you can manage the debt safely. It’s a good idea to check your credit report for errors before applying. Even a small mistake on your file can lower your score. You can find more details on our short term loans page.

Borrowing amongst those with bad credit

Having a poor credit history doesn’t mean you’ll be rejected. Many lenders now prioritise your current financial behaviour over past mistakes. They focus on affordability, looking at whether you can comfortably meet the monthly payments today. For example, a representative APR of 39.9% is often cited for a £2,000 loan over 24 months for those with lower scores. This approach helps people who’ve been turned away by high-street banks whilst they rebuild their credit. If you want to see what options fit your current budget, you can apply for a loan match now.

The role of Open Banking

Open Banking is changing how lenders assess your application. It allows them to see your real-time income and spending patterns securely. This provides a much clearer picture of your financial health than an old credit score alone. “Financial experts suggest Open Banking is revolutionising access for those with lower credit scores.” According to a 2026 report by the Open Banking Implementation Entity, this technology has increased loan approval rates for non-prime borrowers. You can learn more about how your data is protected on the FCA website.

How to apply for a small loan via a credit broker

Applying for small personal loans uk doesn’t have to be a long or stressful process. By using a credit broker, you can simplify your search and find a solution that fits your specific needs. Instead of filling out dozens of forms for different banks, you only need to provide your details once. This method is especially helpful if you’re looking for smaller micro-loans that many high-street banks don’t offer.

The journey follows three simple steps:

- Step 1: Complete a single application form to search a wide panel of lenders simultaneously.

- Step 2: Review the matched offers whilst considering the APR and repayment terms carefully.

- Step 3: Complete the final check with your chosen lender to receive your funds.

Why use a broker like Pixie Loans?

A broker acts as a knowledgeable bridge between you and a network of lenders. Since Pixie Loans is a broker and not a direct lender, we don’t provide the money ourselves. Instead, we use technology to “shop around” for you. This transparency is vital because it saves you the frustration of being rejected by one lender and having to start over. It’s a pragmatic way to see which companies are likely to accept you based on your current financial behaviour.

Final checks and receiving funds

After you’ve been matched and approved, the final stage is straightforward. You’ll usually sign a digital loan agreement, which is much faster than waiting for paperwork in the post. Many lenders in our network aim for efficiency; funds can often be transferred to your bank account on the same day as your approval. If you ever have a dispute that the lender cannot resolve, you can contact the Financial Ombudsman Service for independent help. Always remember to read the fine print before you sign to ensure you’re happy with the commitment.

Taking control of your minor borrowing

Managing an unexpected expense is much easier when you have the right information. We’ve explored how small personal loans uk work as a tactical bridge for short-term needs. By focusing on the total amount repayable and checking your eligibility through Open Banking, you can make a choice that protects your financial health. It’s sensible to use a broker to compare multiple offers whilst avoiding the stress of applying to lenders one by one. This keeps your journey simple and predictable.

If you’re ready to find a solution, we’re here to help you move forward. Pixie Loans provides access to a wide panel of UK lenders and we’re specialists in bad credit matching. We don’t charge you any fees for our service, ensuring you get transparent results. Apply for a small personal loan through Pixie Loans today to see which options fit your current budget. You’ve now got the knowledge to handle this situation with confidence.

Frequently Asked Questions

Can I get a small personal loan with bad credit in the UK?

Yes, you can apply for small personal loans uk even if you have a poor credit history. Many lenders on a broker’s panel specialise in bad credit and focus on your current affordability. They’ll look at your monthly income and outgoings to see if you can safely manage the repayments. This method helps people with lower scores access the funds they need for unexpected life events.

How quickly can I receive a small loan once approved?

You can often receive your funds on the same day that your application is approved. Once you sign the digital agreement, many lenders use faster payments to transfer the money directly into your bank account. In some cases, this can happen within minutes of the final check. This speed is helpful for emergency situations like an urgent car repair or a broken boiler.

What is the minimum amount I can borrow through a credit broker?

The minimum amount you can borrow through a credit broker is typically £100. While many high-street banks set their minimum at £1,000, specialist lenders in a broker’s network cater to those needing smaller sums. This allows you to borrow exactly what you need without taking on extra debt. It’s a sensible way to handle minor, one-off financial challenges like a sudden bill.

Will applying for a small loan affect my credit score?

Applying through a broker uses a soft credit check, which doesn’t affect your credit score at all. This lets you check your eligibility for small personal loans uk without leaving a mark on your record. However, when you move forward with a specific lender for a full application, they’ll perform a hard credit check. This final search will be visible to other lenders on your credit report.

Do I need to provide a guarantor for a small unsecured loan?

You usually don’t need to provide a guarantor for a small unsecured loan. These loans are granted based on your own credit history and your ability to repay from your regular income. If you can show that the monthly instalments are affordable, most lenders will offer the loan to you alone. This makes the process faster as you don’t need to involve anyone else in your finances.