Open Banking Loans: The Future of Fairer Borrowing in the UK

What if your credit eligibility depended on how you manage money today, not one missed payment years ago? If you’ve ever felt the sting of a rejection from a high-street bank despite having a stable income, you aren’t alone. It’s natural to feel frustrated with traditional credit scores that seem stuck in the past. You may also feel anxious about the security of your private data whilst seeking a financial solution.

This article shows how open banking loans are making things fairer for UK borrowers. It focuses on what you can afford right now. We’ll explain how the latest secure API standards reached version 4.0.1 in March 2026. They let you share your information safely. This helps you access products like bad credit loans or debt consolidation loans. You’ll learn how real-time data links you to the credit you need. It keeps the process clear and predictable. It also reflects your current financial health.

Key Takeaways

- Understand how moving from static credit scores to dynamic financial snapshots allows for a more accurate assessment of your current affordability.

- Learn why your data is secure through “read-only” access and API tokens, ensuring you never have to share your actual banking passwords with a lender.

- Discover how open banking loans prioritise your real-time repayment behaviour, offering a fairer path to credit for those with a less-than-perfect history.

- Find out how to prepare your primary bank account for an application by reviewing your recent transaction behaviour for potential red flags.

- See how using a credit broker can simplify your search by connecting you with multiple lenders who value transparency and modern data sharing.

Table of Contents

Beyond the Credit Score: The Rise of Open Banking Loans in the UK

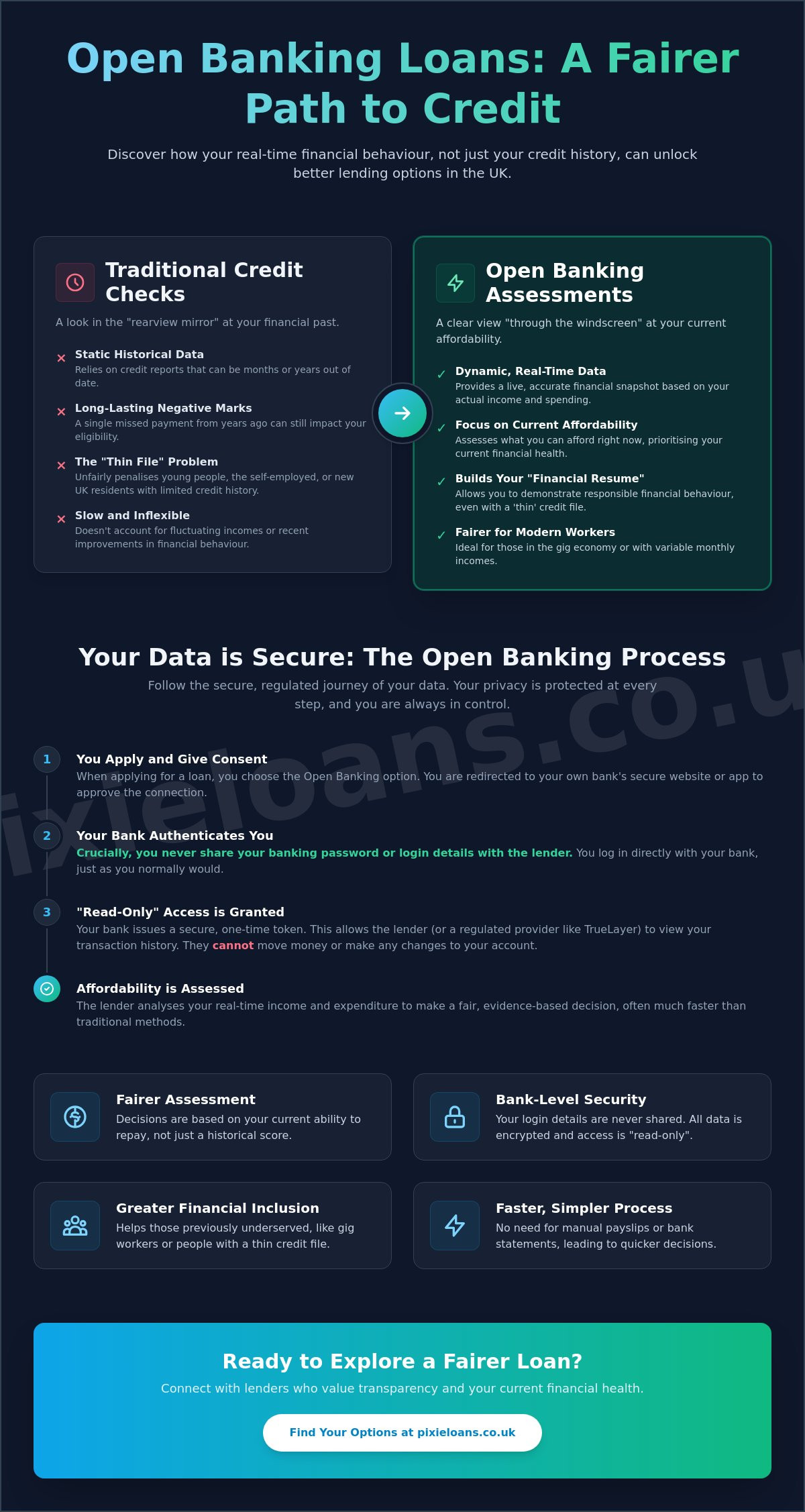

Traditional credit scoring often feels like looking in a rearview mirror. It relies on historical data that might be months or even years out of date. If you’ve ever missed a payment during a difficult period, that single event can shadow your financial life for years. Open banking loans represent a shift toward looking through the windscreen instead. These products use real-time transaction data to assess what you can afford today, rather than what you struggled with yesterday.

If you’re wondering, What is Open Banking? it’s essentially a secure way for you to give lenders permission to view your bank statements digitally. Traditional credit reports are "static" documents; they’re snapshots taken at a specific point in time. In contrast, open banking loans rely on "dynamic" data. This means a lender sees a living history of your finances. For modern UK workers in the gig economy or those with fluctuating monthly incomes, this is vital. If your earnings vary but your ability to manage expenses remains strong, a dynamic assessment reflects that reality in a way a traditional score simply cannot.

The Financial Conduct Authority (FCA) and the Joint Regulatory Oversight Committee (JROC) have been instrumental in standardising this technology. By March 2026, the release of version 4.0.1 of the Open Banking API specifications ensured that data sharing is more granular and secure than ever before. This regulatory framework means the technology isn’t just a trend; it’s a robust, consumer-protected standard designed to improve financial inclusion across the UK lending market.

The "Thin File" Problem in the UK

Many young people, self-employed contractors, or new UK residents face a common hurdle: the "thin file." If you don’t have a long history of credit cards or mortgages, traditional algorithms often label you as high risk by default. Open banking changes this by allowing you to present a "financial resume" based on your actual income and spending patterns. It helps prove that you’re a responsible borrower through your current behaviour, which is a significant step forward for millions of UK adults who were previously underserved by high-street institutions.

Why 2026 is the Year of Open Data

We’ve moved past the initial trial phases of open data. In 2026, the maturation of the ecosystem means there are more Account Information Service Providers (AISPs) than ever. Lenders are now prioritising affordability over simple credit scores because real-time data allows them to manage risk more effectively. If a lender can see your consistent salary deposits and how you manage your monthly utilities, they can offer products like bad credit loans or unsecured loans with greater confidence. This shift helps move the industry away from regional biases and toward individual merit.

How Open Banking Works: Security, Consent, and Data Sharing

One of the most common concerns for anyone considering open banking loans is the safety of their financial data. It’s a valid worry. However, the system is built on a "Read-Only" foundation. This means that when you grant a lender access, they can only view your transaction history to assess affordability. They cannot move your money, set up payments, or make any changes to your account. You remain the gatekeeper of your funds at all times.

The security of this process relies on API tokens rather than your banking credentials. When you apply for a loan, you aren’t giving your password to the lender or a middleman. Instead, you’re redirected to your own bank’s secure app or website to authorise the connection. Once you log in there, your bank issues a secure, encrypted token that allows the lender to view specific data points. This method ensures your sensitive login details never leave the safety of your bank’s own environment.

All data shared through this process is encrypted to the same high standards used by major financial institutions. These protections are underpinned by the UK’s Open Banking regulations, which mandate strict technical requirements for every participant. If you’re ready to see how this secure technology can assist your search for credit, exploring your options through a broker is a sensible first step to find a suitable match.

The Role of the AISP

You might notice names like TrueLayer or AccountScore during your application. These are Account Information Service Providers (AISPs). They act as regulated middlemen that safely transport data between your bank and the lender. Every AISP must be authorised and regulated by the Financial Conduct Authority (FCA). You can easily verify any provider by checking their name on the official FCA Register, providing an extra layer of peace of mind before you proceed.

Staying in Control: Revoking Access

Your consent is never permanent. Under current rules, any permission you grant for ongoing data access automatically expires after 90 days. However, you don’t have to wait that long. You can revoke access at any moment through your own banking app’s "connected apps" or "security" settings. Once you withdraw consent, the lender’s digital key is instantly destroyed. Furthermore, under UK GDPR, you have the "Right to be Forgotten," meaning you can request that a lender deletes your shared data once the assessment or loan term is complete.

Why Open Banking is Revolutionising Lending for Bad Credit

If your credit file contains defaults or late payments from several years ago, you’ve likely faced rejection from high-street banks. These institutions often rely on rigid algorithms that don’t account for how your life has changed. Open banking loans disrupt this cycle by prioritising your current "repayment capability" over your past mistakes. By sharing a digital snapshot of your recent transactions, you provide proof that you can manage a new commitment today, regardless of what happened in the past.

The efficiency of this technology is a significant advantage for those with less-than-perfect history. In the past, assessing a complex application meant days of manual bank statement reviews and physical paperwork. Now, the process happens in seconds. This speed doesn’t just benefit the lender’s operations; it provides you with a near-instant answer, reducing the anxiety often associated with applying for credit. If you’ve been stuck in a loop of waiting and wondering, this real-time approach offers a much-needed change of pace.

This approach also helps dismantle "postcode lending" and other regional biases. Traditional credit models sometimes penalise individuals based on where they live or the demographic data of their neighbours. By focusing purely on your individual bank account, lenders can offer more personalised rates. This helps reduce the "poverty premium," where those with lower credit scores are often forced to pay significantly more for credit even if they have a stable, manageable budget. This shift aligns with the regulator’s broader vision for open finance, which aims to empower consumers through better data utility.

Categorisation: How AI Reads Your Statement

Lenders use sophisticated software to categorise your spending patterns. It’s helpful to understand that they aren’t looking to judge your lifestyle choices. Instead, the technology distinguishes between essential bills, like rent and utilities, and discretionary spend. If a lender sees a consistent "stable income" signal and that your essential costs are covered, a few "favourite" luxuries won’t necessarily lead to a rejection. They simply want to see that you have a surplus at the end of the month to safely cover loan repayments.

Fairer Outcomes for Debt Consolidation

For those seeking debt consolidation loans, open banking provides a level of accuracy that manual forms cannot match. It allows the lender to verify your total debt load and current repayment schedule with precision. If the data shows that a new, single monthly payment will be lower than your current combined outgoings, it makes the case for affordability much stronger. There is also a psychological benefit; knowing that an assessment is based on your actual, current efforts to stay on top of your finances can make the borrowing journey feel far more respectful and fair.

Preparing for an Open Banking Loan Application

Preparing for open banking loans is less about gathering physical paperwork and more about ensuring your digital footprint is accurate. Because the lender sees a live feed of your transactions, you must be strategic about which account you connect. If you share a secondary account with little activity, the lender won’t have enough data to make an informed decision. You should always connect the account where your salary is paid and your main household bills are settled. This provides the clearest picture of your actual disposable income.

This technology effectively acts as a "truth machine." It’s impossible to hide undisclosed debts or other financial commitments when a lender has a direct view of your bank statement. If you have existing short term loans or other credit repayments, they’ll be visible. Honesty is vital here. Providing an accurate picture of your finances from the start ensures that any product you’re matched with is truly affordable for your specific circumstances. If you’re considering a smaller amount to cover an unexpected expense, our guide to securing a £200 loan safely and affordably can help you understand your options before you apply.

Lenders also look for patterns of stability. Frequent transactions to gambling sites or large, unexplained cash withdrawals can be viewed as red flags during the automated assessment. If you’re planning to apply, searching for a loan through a broker after a period of steady, predictable financial behaviour can significantly improve your chances of finding a suitable match.

Digital Housekeeping Before You Apply

It’s sensible to organise your finances at least 30 days before making a major application. You might consider closing unused bank accounts that could clutter your financial snapshot or confuse the categorisation software. Using a budgeting app in the months leading up to your application can also help "train" your data. If your bank’s own app allows you to categorise spending, ensure your rent and utility payments are correctly labelled so the lender’s AI recognises them as essential commitments immediately.

Common Pitfalls to Avoid

One of the biggest mistakes is attempting to "game" the system. Moving money rapidly between different accounts to inflate your balance, often called "cycling," is easily spotted by modern algorithms and can lead to an instant rejection. You should also check that your specific bank fully supports the lender’s chosen AISP before you begin. If the connection fails, it can delay your application. Finally, don’t forget to check your balance; if an account is constantly in its overdraft, it may signal to a lender that you’re struggling to manage your current outgoings.

Using a Credit Broker to Navigate Open Banking Options

Finding the right financial product shouldn’t feel like a game of chance. Whilst a direct lender offers a single path with one set of criteria, using a credit broker allows you to explore a wider range of open banking loans through a single, secure application. This approach is particularly beneficial if you’re concerned about your credit history. Instead of sharing your data multiple times with different companies, a broker acts as a central hub. You provide one digital connection, and the technology does the work of identifying which lenders on our panel are most likely to accept your request based on your real-time affordability.

The transparency of the broker model is a vital component of the UK credit market. It shifts the power back to the consumer by providing a clear view of available options without the need for repetitive data entry. By using a broker, you benefit from a structured process that values your time and your financial privacy. The goal is to create a knowledgeable bridge between your specific needs and the lenders who are best equipped to meet them. This ensures that open banking loans are matched with borrowers who can truly afford them, protecting both the lender and your own long-term financial stability.

Efficiency and Personalisation

Efficiency is at the heart of the broker model. By using the categorised data from your bank account, a broker can filter out lenders whose criteria you don’t meet before a formal application is even made. This significantly reduces "application fatigue" and helps you find a match more quickly. Most importantly, brokers typically use "soft searches" to check your eligibility. This means you can see your options for short term loans, bad credit loans, or unsecured loans without leaving a mark on your credit file that other lenders can see. This same soft-search approach is equally useful when you need a smaller sum, such as a £200 loan to cover an urgent unexpected cost, allowing you to compare options without affecting your credit score.

-

One Application: Access multiple lenders with a single data share.

-

Soft Searches: Explore your eligibility without impacting your credit score.

-

Precision Matching: Technology filters lenders based on your actual transaction history.

Your Next Steps with Pixie Loans

At Pixie Loans, we’ve designed our process to be as transparent and straightforward as possible. When you begin your application, you’ll be given the option to connect your bank account securely via our regulated partners. If you choose to proceed, the system will categorise your income and expenditure in seconds. Once this data share is successful, you’ll typically receive a response from our panel within minutes. We prioritise your financial health by matching you with trusted lenders who value the transparency of open data. This ensures that if a loan is offered, it’s because the lender is confident it fits comfortably within your current monthly budget.

Embracing a More Transparent Financial Future

Open banking represents a significant shift in how the UK credit market evaluates suitability. By prioritising your current financial health over past mistakes, these tools provide a more accurate picture of what you can comfortably afford today. We’ve explored how secure, read-only access protects your data whilst giving you the opportunity to prove your reliability through real-time behaviour. This modern approach to open banking loans ensures that your application is judged on its individual merits rather than an outdated, static algorithm.

As an FCA-regulated credit broker, Pixie Loans is here to help you navigate this evolving landscape with confidence. We use secure bank-level encryption to connect you with a wide panel of trusted UK lenders, ensuring your information remains protected throughout the search process. Find a fairer loan match today with Pixie Loans. Taking control of your financial journey starts with choosing a path that values your actual progress and current affordability. We’re ready to help you find the solution that fits your life right now.

Frequently Asked Questions

Is open banking safe for loan applications in the UK?

Yes, open banking is very safe for loan applications as it operates under strict FCA regulations and uses the same security protocols as your bank. Data is shared via encrypted API tokens, which means your sensitive information is never exposed to unauthorised parties. Because the system is "read-only," no lender can move money or change your account settings; they can only view the data you’ve specifically permitted.

Can a lender see my bank password if I use open banking?

No, a lender will never see or store your bank password. When you apply for open banking loans, the process redirects you to your own bank’s secure login page or mobile app. You enter your credentials there, and your bank sends a secure digital token to the lender. This ensures that your login details remain strictly between you and your bank.

Does using open banking affect my credit score?

Sharing your data through open banking does not affect your credit score. The process of connecting your account is a data-sharing activity, not a credit event. However, the lender may still perform a traditional credit search as part of your application. If they do a "hard search," that will appear on your report, but the actual use of open banking technology is entirely neutral for your score.

Can I refuse to use open banking when applying for a loan?

You can certainly refuse to use open banking, as it is an optional, consent-based service. If you prefer not to share digital access, some lenders may allow you to provide manual bank statements instead. It’s worth noting that some specialist lenders may require open banking to accurately assess your affordability, so refusing might limit the number of loan products available to you.

What data can lenders actually see through open banking?

Lenders can see your transaction history, account balance, and account holder name. This includes your regular income, such as salary or benefits, and your outgoing expenses like rent, utilities, and other credit repayments. They use this information to build a clear picture of your disposable income. They cannot see your login credentials or access other products you might have with that bank, like savings or mortgages, unless you specifically authorise it.

How long does a lender have access to my bank account?

For most loan applications, the lender only needs a one-off snapshot of your recent transaction history, typically covering the last 90 to 180 days. If you grant ongoing access, UK regulations state that this consent automatically expires after 90 days. You don’t have to wait for this limit to pass; you can check which companies have access and end the connection through your bank’s security settings whenever you choose.

Will a lender reject me if they see I spend money on gambling or takeaways?

Occasional spending on luxuries like takeaways won’t usually lead to a rejection. Lenders are primarily looking for proof that you have enough surplus income to cover the loan repayments after your essential bills are paid. However, frequent and heavy spending on gambling or persistent reliance on an unarranged overdraft can be seen as signs of financial stress, which might affect the lender’s decision on your affordability.

Can I revoke access to my bank data after the loan is approved?

Yes, you can revoke access to your bank data at any time, even after your loan is approved and funded. You can do this easily through your banking app or by contacting your bank directly. Once you withdraw your consent, the lender’s digital key is deactivated immediately. This allows you to maintain full control over your privacy throughout the duration of your open banking loans and beyond.

Related links

How to check if Facebook handed your data over to Cambridge Analytica