Use Payday Loans Safely: A Guide to Avoiding Debt Traps

Estimated reading time: 10 minutes

Takeaways

- Payday loans offer quick cash but come with high interest rates, reaching up to 1,500% APR.

- You can borrow between £50 and £1,000, with repayment required by your next payday, but be cautious of debt traps.

- To use payday loans safely, only borrow what you can afford, ensure the lender is FCA approved, and compare rates.

- Explore alternatives to payday loans, such as credit unions or arranged overdrafts, to avoid costly borrowing mistakes.

- Always know your rights as a borrower and understand Continuous Payment Authority to protect your financial wellbeing.

Table of contents

Payday loans rank among the costliest ways to borrow money, with interest rates soaring up to 1,500% APR. Quick cash loans may seem helpful for urgent expenses. However, they can lead to a tough cycle of debt for borrowers if you do not use payday loan safely.

In general, a payday loan lets you borrow £50 to £1000, which you must repay with interest on your next payday or shortly after. Lenders typically need your bank details to collect payments through a “continuous payment authority” (CPA). Furthermore, the law provides key protections for people who take out loans.

For example, since January 2015, daily interest rates can’t go over 0.8%. Borrowers also don’t have to pay back more than twice what they borrowed. Therefore, a 30-day loan repaid on schedule should not incur more than £24 in fees and charges per £100 borrowed.

Equally, you should think over your options carefully before searching how to get a payday loan or seeking quick cash. This piece helps you direct through the payday loan world safely. Also, you’ll discover better alternatives and learn to avoid common pitfalls that push many borrowers into financial troubles.

What is a Payday Loan and How Does it Work?

A payday loan works as a short-term cash advance between £50 and £1,000. That is to say, these financial products help you get money between paychecks. They also give you quick cash for unexpected costs.

Short-term borrowing explained

Likewise, payday loans are unsecured loans that let you get small amounts of money quickly when you need it. The name “payday” comes from the expectation that you’ll pay back the money on your next payday.

To begin with, lenders make verification easy. Some check your income using pay stubs and bank statements. Others might not check your income or credit at all. Overall, you can get these loans easier than regular bank loans, especially if you have trouble getting normal credit.

How quick payday loans are repaid

Your repayment method depends on whether you get a loan in-store or online:

- At retail stores, you write a postdated cheque for the full amount plus fees

- Online loans send funds directly to your account

- Most people authorise a Continuous Payment Authority (CPA), which lets the lender take money from your bank account automatically

You usually have up to one month to repay what you borrowed plus interest. If there isn’t enough money in your account when payments are due, lenders may try to collect part of the payment. However, there are rules that limit how often they can do this.

Why interest rates are so high

Payday loans cost by a lot more than other types of credit because:

- Lenders say regular interest rates wouldn’t make money on small, short-term amounts

- A £79.42 one-week loan at 20% APR would only make 38 pence in interest

- Lenders can’t patent their loans, so they have no reason to lower prices

With this intention, most payday lenders charge the highest rates allowed by law, which often reach 400% APR or more. These loans remain expensive even after the 2015 cap of 0.8% daily interest.

The Real Risks of Payday Loans UK

A quick payday loan might look like a quick solution to your money problems. Then again, the risks are more than just high interest rates. You need to know about these risks before you sign any contract.

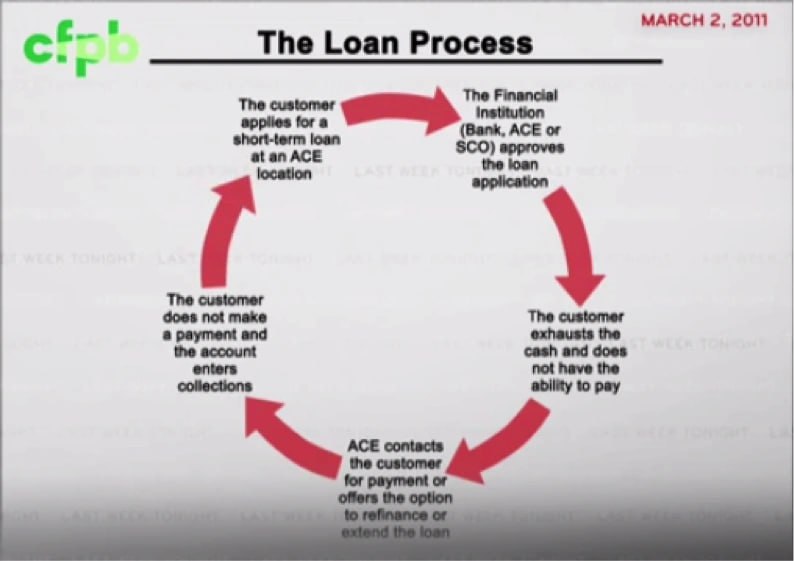

How debt traps start

The debt trap starts simply enough. You borrow money for an emergency and plan to pay it back with your next paycheck. Even so, breaking free from this cycle becomes a real challenge. Payday lenders get 75% of their fees from people who take out 10 or more loans each year.

All but one of these loans get rolled over or renewed. In other words, borrowers keep taking new loans to pay off old ones. The average person stays in debt for five months and pays £412.96 in fees to borrow just £297.81.

Effect on your credit score

Payday loans don’t usually show up on major credit reports at first. However, your credit file still keeps these loans on record for six years. Paying on time won’t hurt your score much, but having payday loans in your history can limit your future borrowing options.

For one thing, many mortgage companies won’t accept applications from people who have a history of payday loans. This applies even if they paid them back on time. Lenders see payday borrowing as a warning sign of money management problems.

What happens if you miss a payment

In the long run, missing payments creates a chain of problems. Lenders can charge a default fee (the FCA caps this at £15). Your balance grows as interest keeps adding up.

In due time, lenders may sell unpaid debts to collection agencies, resulting in legal action in serious cases. Additionally, your bank could also hit you with overdraft fees if automatic payments fail.

Understanding continuous payment authority (CPA)

Presently, payday lenders usually use CPA to take repayments straight from your account. CPAs give you less protection than direct debits. Moreover, lenders can try multiple withdrawals whenever they think payment is due.

With this in mind, you have the right to cancel a CPA by calling your bank before the end of business day before your scheduled payment. The law protects this cancellation right, but many borrowers don’t know about it.

How to Use Payday Loans Safely

You need to know how to handle payday loans safely to avoid money problems. Smart borrowing begins with good planning and staying aware of what you’re getting into.

Only borrow what you can repay

While the temptation to borrow extra money is strong, this often makes repayment tough. Start by making a budget to figure out your exact needs and what you can actually pay back. For this reason, use payday loans just for basic needs—not holidays, home improvements, or paying off other debts. Take a good look at whether your next paycheck will cover the loan plus interest without leaving you broke again.

Check if the lender is FCA approved

The Financial Conduct Authority (FCA) must oversee all reliable payday lenders. Before you apply, check the lender is on the Financial Services Register at register.fca.org.uk. In particular, watch out for loan offers that come to you—these are usually scams. Also, don’t pay any upfront fees for loan applications, as real lenders won’t ask for these.

Compare payday loans online for better rates

For the most part, interest rates can differ vastly between lenders, and comparing them could save you good money. You’ll often see a big difference between the cheapest and most expensive loans. Some lenders focus on specific loan types, which might make them cheaper for what you need. Start by using trusted comparison websites to find the lowest APR that works for you.

Avoid rollovers and hidden fees

At the same time, getting a rollover loan to extend your repayment deadline may look like a good idea, but it often ends up costing you more. The FCA rules state that lenders are not allowed to roll over loans more than twice. The lender should clearly show all costs upfront. In addition, daily interest can’t go above 0.8%, and total repayment (including interest and fees) stops at 100% of the loan amount.

Know your rights as a borrower

It’s important to realise that you can cancel a Continuous Payment Authority (CPA). In this situation, you can inform your bank one day before payment is due. In the first place, lenders need to check if you can afford the loan before they approve it. If you have trouble paying back your loans, lenders should direct you to free debt help services.

Better Alternatives to Payday Loans

A point often overlooked is that you have better options than expensive payday loans that won’t trap you in debt cycles.

Low interest payday loans from credit unions

Firstly, credit unions provide loans with interest rates capped at 3% monthly. These rates are nowhere near payday lenders’ 400% APR or more. That is to say, credit unions are not-for-profit financial groups.

They care more about their members’ wellbeing than making money. They offer tailored financial advice and flexible repayment options during tough times.

Using an arranged overdraft

Secondly, bank arranged overdrafts cost less than payday loans. A £100 loan through HSBC’s planned overdraft would cost £1.40 for 28 days, while a payday loan could reach £22.40. Setting up overdrafts beforehand helps prevent extra borrowing fees.

Asking family or friends for help

At the same time, money from people you know comes without interest charges. Create a budget that shows your repayment plan before you ask. For this reason, written agreements help keep good relationships. Equally, talk about missed payments before they happen.

Government grants or emergency support

Local Welfare Assistance schemes give emergency financial help that you don’t need to repay. Your location might qualify you for:

- Emergency Assistance Payments (Wales)

- Community Care Grants (Scotland)

- Discretionary Support (Northern Ireland)

Debt consolidation loans as a long-term fix

Finally, consolidation loans merge multiple debts into one monthly payment. This option works best after you understand why the debt happened. Notably, success needs discipline to avoid new debts and pay off what you owe.

Conclusion

Payday loans give you quick cash during emergencies but come with major risks that lead to long-term money problems. These loans rank among the costliest borrowing options with interest rates that can hit 1,500% APR.

In particular, you should explore alternatives before turning to payday loans. As shown above, credit unions, arranged overdrafts, family loans, government assistance, and debt consolidation are much more affordable options. These choices will save you hundreds of pounds in interest and help you stay clear of the debt cycle.

All in all, if you need a payday loan, keep these important tips in mind: Only take what you can afford to pay back. Make sure the lender is FCA approved. Compare rates from different lenders. Avoid rollovers. Know your rights as a borrower. Finally, you should understand how Continuous Payment Authority works.

Your financial wellbeing is too valuable to risk falling into a debt trap. Most payday loan users need multiple loans to cover their expenses and stay in debt for months. In short, this pattern shows why payday loans should be your last option.

All in all, smart borrowing requires looking beyond quick fixes. Payday loans might fix today’s problem but create bigger ones later.

Ultimately, financial stability comes when you make wise decisions about borrowing and understand the true costs. Make wise decisions to protect your financial future.

Related links