How to Get a Loan for a New Kitchen: A Practical UK Guide for 2026

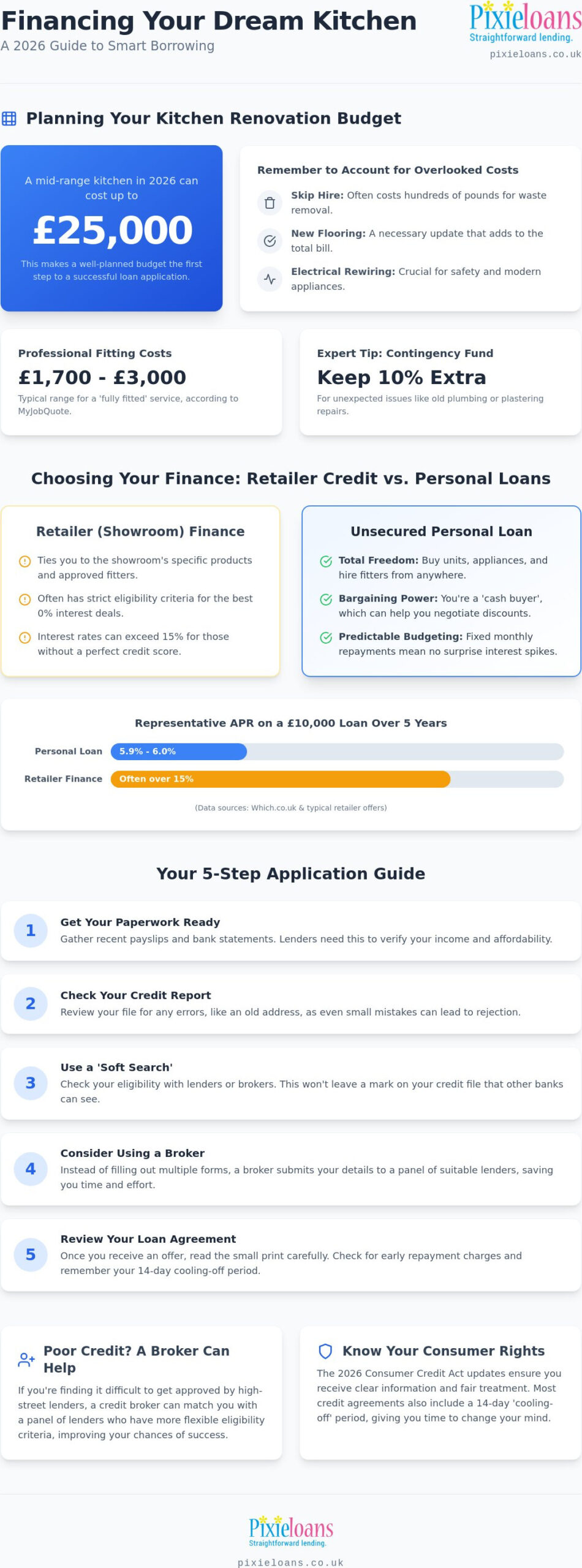

Did you know a mid-range kitchen in 2026 can cost up to £25,000? We agree that building your dream space is a big step that often feels out of reach. If you are wondering how to get a loan for a new kitchen, we’re here to help. We promise to show you the most effective ways to finance your build whilst keeping payments affordable. We’ll compare flexible personal loans against retailer credit so you can start your home renovation with total confidence and clarity.

Key Takeaways

- Identify your total project costs by accounting for often-overlooked expenses like skip hire, flooring, and professional electrical rewiring.

- Analyse the differences between retailer finance and personal loans to decide which option offers the best flexibility for your chosen fitters.

- Master the practical steps of how to get a loan for a new kitchen by preparing your financial documents and credit report in advance.

- Explore how working with a credit broker can help you find suitable lenders if high-street showrooms have strict eligibility criteria.

- Use the 2026 Consumer Credit Act updates to ensure you receive clear information and fair treatment throughout your borrowing journey.

Planning Your Kitchen Renovation Budget in 2026

Starting a kitchen project is exciting, but the numbers can feel overwhelming. Understanding how to get a loan for a new kitchen begins with a clear spreadsheet. You need to identify every cost, from the cabinetry and appliances to professional installation fees. Don’t forget hidden expenses like skip hire, which often costs hundreds of pounds, or new flooring and electrical rewiring. A well-planned budget is the first step toward a successful loan application. It shows lenders you’re a responsible borrower who has considered the full project scope before seeking funds.

Estimating the Full Cost of Installation

When you browse showrooms, you’ll see “supply-only” and “fully fitted” quotes. Supply-only covers the units, whilst fully fitted includes labour. According to MyJobQuote, fitting costs in 2026 typically range from £1,700 to £3,000. It’s wise to keep a 10% contingency fund for surprises. You might find old plumbing needs replacing or walls need extra plastering once the old units come down. These unexpected issues can quickly drain your savings if you haven’t planned for them in your initial borrowing request.

Setting Your Financial Boundaries

Before you commit, it’s helpful to understand what a loan is and how interest impacts your total debt. Use our loan calculator to model different repayment scenarios. This tool helps you evaluate your disposable income whilst accounting for potential interest rate changes. With average rates on a £10,000 loan sitting around 8.0%, you must ensure the monthly payment fits comfortably in your lifestyle. Be honest about what you can afford so your dream kitchen doesn’t become a financial burden in the years ahead.

Comparing Kitchen Finance: Retailer Credit vs Personal Loans

Many homeowners wonder if showroom finance is the only path. Whilst 0% interest deals look attractive, they often come with strict eligibility criteria. If you are looking at how to get a loan for a new kitchen, an independent personal loan might offer more freedom. This choice lets you buy cabinets from one supplier and appliances from another. The UK government is modernising the Consumer Credit Act in 2026 to provide you with clearer information and more protection during your renovation journey.

Showroom Credit vs Independent Loans

Showroom credit often ties you to their specific fitters. In contrast, bank-issued unsecured loans don’t require you to use your home as collateral. You receive the funds directly, which simplifies the process. According to Which.co.uk, representative APRs for a £10,000 loan over five years are currently around 5.9% to 6.0%. This is often lower than the interest rates charged by retailers, which can exceed 15% for those without perfect credit. The official guide to personal loans provides a clear breakdown of how these products work.

The Flexibility of Unsecured Personal Loans

When the loan amount hits your bank account, you become a ‘cash buyer’. This status gives you significant bargaining power with independent local fitters who might offer discounts for prompt payment. It also helps with long-term budgeting. Fixed monthly repayments mean you know exactly what’s leaving your account each month. Understanding how to get a loan for a new kitchen with fixed rates helps you avoid future interest spikes. If you’re ready to see what’s available, you can start your application journey today to compare different lenders.

How to Apply for a Kitchen Loan: A Step-by-Step Guide

Applying for a kitchen loan is much easier when you’re organised. Start by gathering your payslips and recent bank statements. Lenders need this proof of income to confirm you can afford the monthly repayments. You should also check your credit report for errors. Even a small mistake on your address can lead to a rejection. Learning how to get a loan for a new kitchen involves understanding the digital application process. Using a broker can save you time. Instead of filling out multiple forms, you submit your details once. The broker then matches you with a panel of lenders who are likely to accept your application. You can compare home improvement loans to see how different products stack up against your budget.

Checking Your Eligibility Without Affecting Your Credit Score

Many people worry that checking for a loan will hurt their credit score. This is where “soft” searches come in. A soft search lets a lender look at your file without leaving a mark that other banks can see. It’s a great way to see your chances of approval. You can check your emergency loan eligibility as a quick first step to see where you stand. Once you find a suitable match, the lender will perform a “hard” check during the final application phase.

Finalising Your Loan Agreement

When you receive an offer, read the small print carefully. Look for early repayment charges. Some lenders charge you if you pay the loan off sooner than planned. UK law also provides a 14-day cooling-off period for most credit agreements. This gives you time to change your mind if you decide the project isn’t right. If you want to know how to get a loan for a new kitchen quickly, ensure your digital documents are ready for upload. Check the total cost of credit. This number tells you exactly how much you’ll pay back in total, including all interest and fees. After you’re happy, you can complete your application online to get started.

Securing a Loan with Poor Credit: How a Broker Can Help

If you’ve been turned down by a high-street showroom, don’t lose hope. Many major retailers have very strict credit requirements for their 0% interest deals. This can be frustrating when you’re simply trying to improve your home. Understanding how to get a loan for a new kitchen when your credit score isn’t perfect is about looking at different options. A credit broker acts as a pragmatic facilitator. Instead of rejecting you based on a single number, they work with a panel of lenders who provide loans for bad credit.

Why Use Pixie Loans to Find Your Kitchen Finance

Filling out dozens of forms is exhausting. With Pixie Loans, you use a single application form to reach multiple potential lenders at once. It’s a common-sense approach that saves you time and protects your credit file from unnecessary hard searches. We believe in transparency and honest guidance. If a lender can help, they’ll show you the terms clearly. This method ensures you find a monthly payment that fits your budget without the stress of visiting every bank on the high street just to be rejected.

Focusing on Affordability in 2026

Modern lending in 2026 focuses on affordability checks rather than just your past mistakes. According to Finder, average interest rates for a £5,000 loan were 10.05% in February 2026. Lenders want to see that your current income can cover these costs comfortably. New FCA regulations arriving in July 2026 also ensure better protection for borrowers. If you’re still figuring out how to get a loan for a new kitchen, remember that your current financial health is what matters most to specialist lenders today.

Taking the Next Step Toward Your Dream Kitchen

Success starts with choosing the right financing. By understanding how to get a loan for a new kitchen, you avoid restrictive showroom terms. Our service offers quick matching with a panel of UK lenders and soft-search eligibility checks. We are specialists in bad credit loan solutions, providing a common-sense bridge to your goals. Start your kitchen loan application with Pixie Loans today to begin your renovation. As experts at Checkatrade note, a quality kitchen adds real value to your home. We’re here to help you every step of the way.

Frequently Asked Questions

Can I get a kitchen loan if I have a bad credit history?

Yes, you can. Modern lenders prioritising affordability over old scores help many homeowners. As one financial expert notes, “Your current ability to repay is now the primary focus for specialist lenders.” This means you can still secure funds even if high-street banks have turned you down previously. We specialise in connecting you with these flexible providers who look at your whole situation.

Is it better to use retailer finance or a personal loan for a kitchen?

Personal loans usually offer more freedom. If you learn how to get a loan for a new kitchen independently, you aren’t forced to use a showroom’s expensive installation team. “Choosing an independent loan gives you the power to negotiate with local tradespeople,” explains a kitchen design consultant. This often results in a lower total project cost whilst giving you control over the build.

How much can I typically borrow for a new kitchen in the UK?

Most unsecured lenders offer up to £35,000. Data from Homebuilding & Renovating shows units for large kitchens can cost up to £9,100. When calculating your request, remember to include fitting and plumbing labour. “Borrowers should always factor in a 10% safety net for structural surprises,” advises a leading property developer. This ensures you have enough funds to finish the job properly.

Will applying for a kitchen loan affect my credit score?

Initial soft-search checks won’t affect your score. Only a full, formal application involves a “hard” search that stays on your report. “Soft searches are a vital tool for consumers to compare rates safely,” states a report from the FCA. By using these checks, you can explore how to get a loan for a new kitchen without damaging your future borrowing potential.

How long does it take to get the money from a kitchen loan?

Most funds are released within 24 to 48 hours of approval. Once you sign your digital agreement, the transfer is often near-instant. “Speed of delivery is a hallmark of modern fintech lending,” says a digital banking analyst. This fast turnaround allows you to pay deposits to fitters and order your materials immediately, keeping your renovation timeline on track for a quick finish.