Home Improvement Loan for Bad Credit: A 2026 UK Buying Guide

Why should a past financial mistake prevent you from fixing a leaking roof or a broken boiler today? If you’ve been turned away by high street banks, you aren’t alone. It’s frustrating when your credit history stops you from maintaining your property. Finding a home improvement loan for bad credit can feel like an uphill battle, especially when you need urgent repairs. We believe your current ability to afford repayments is what matters most. You deserve a clear path to a safer, more comfortable home.

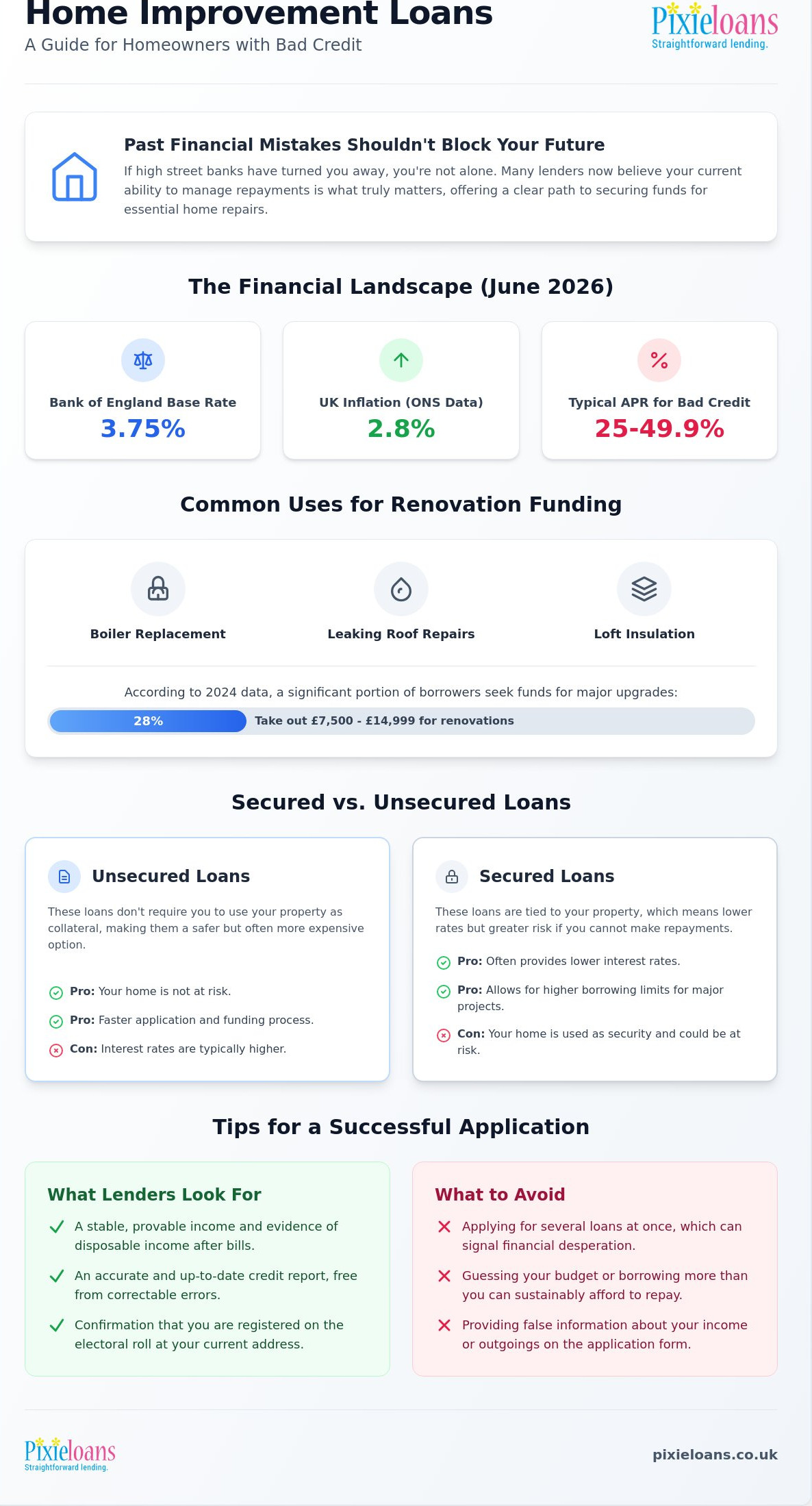

This guide explains how to secure renovation funds by focusing on affordability. With the Bank of England base rate at 3.75% as of June 2026, the market is shifting. While APRs for these products can range from 25% to 49.9%, new FCA proposals from June 2026 help lenders assess your full financial situation. According to ONS data, UK inflation is 2.8%. As a broker, we’ll help you navigate the application process to find a lender that values your current budget over your history.

Key Takeaways

- Learn how a home improvement loan for bad credit can help you fund essential repairs like boiler replacements even if your history isn’t perfect.

- Discover why lenders in 2026 prioritise your current monthly affordability over past financial mistakes when assessing your application.

- Understand the critical differences between secured and unsecured borrowing to protect your property whilst securing the best possible rates.

- Find out how a streamlined broker service can quickly connect you with specialist lenders who look beyond your credit score.

What is a Home Improvement Loan for Bad Credit?

A home improvement loan for bad credit is a specific financial product designed to fund property renovations when your credit score is low. If you’ve faced rejections from high-street banks due to past defaults or CCJs, these loans offer a second chance. They provide the capital needed to upgrade your living space, serving as a vital tool for property value enhancement despite a less-than-perfect credit history. For property investors managing larger commercial projects, you can learn more about JGL Capital LLC to discover how asset-backed loans can help. You don’t have to let your past financial behaviour stop you from creating a better home for your family.

Bridging the Gap for Low Credit Scores

Traditional lenders often use automated systems that instantly decline anyone with a low score. Specialist lenders are different because they look at your current affordability. They want to see if you can manage the monthly payments today, regardless of what happened years ago. This approach makes it easier to get the cash you need for vital repairs. It’s a supportive way to help homeowners maintain their properties without the stress of constant rejection from mainstream banks.

How a Credit Broker Helps You Find a Loan

A broker like Pixie Loans acts as a bridge between you and multiple specialist lenders. They scan a wide panel to find firms most likely to accept your specific credit profile. This saves you time and prevents multiple hard searches on your file. They might also help you explore Guarantor Loans. Having a friend or family member back your application can significantly increase your chances of securing a competitive rate.

Common Uses for Renovation Funding

Many borrowers use these funds for essential repairs. For example, replacing an old boiler or fixing a leaking roof prevents further damage. According to 2024 data, 28% of borrowers take out between £7,500 and £14,999 for home renovations. You could also invest in energy-efficient upgrades like loft insulation. These improvements don’t just make your home more comfortable; they can also lower your energy bills. It’s a smart way to invest in your property’s future whilst improving your daily life, and using professional support like Pink Lady Cleaning Services can help you maintain those high standards at home.

Eligibility and Improving Your Chances of Approval

In 2026, lenders have shifted their focus significantly. They now look at your current affordability rather than just your past credit mistakes. To qualify for a home improvement loan for bad credit, you need to be a UK resident and at least 18 years old. Having a stable income is the best way to show you can handle the monthly cost. Lenders specifically look for ‘disposable income’ after all your monthly bills are paid to ensure the loan is sustainable.

Actionable Tips for a Successful Application

You can improve your odds by being prepared. Check your credit report for any errors before you apply. Even a tiny mistake can drag your score down. It’s also helpful to make sure you’re on the electoral roll at your current home. This makes it much easier for lenders to verify who you are. When you fill out your form, be honest about your spending. Clear details about your outgoings help lenders see that you’re a responsible borrower.

What to Avoid When Borrowing with Poor Credit

Don’t apply for several loans at once. This can make you look desperate for cash and might hurt your score further. It’s also vital that you don’t guess your budget when looking for a home improvement loan for bad credit. Use a loan calculator to see what fits your lifestyle. If you’re renovating for accessibility, look into UK Government Disabled Facilities Grants as these aren’t based on credit. Never lie about your wages, as this leads to an instant “no”. When you’re prepared, you can complete an enquiry form to explore your options.

Comparing Unsecured and Secured Home Improvement Loans

Deciding on the right loan type is a balance of risk and reward. An unsecured home improvement loan for bad credit doesn’t require you to use your property as collateral. This keeps your home safe if your financial circumstances change unexpectedly. On the other hand, secured loans often provide lower interest rates because the lender has the security of your property. Whilst unsecured loans are typically funded much faster, secured options offer the higher limits needed for major building works.

The Pros and Cons of Unsecured Personal Loans

Speed is the main benefit of an unsecured agreement. You won’t need a professional home valuation, which can save weeks of waiting time. This is particularly helpful if you’re dealing with an emergency like a broken heating system. The downside is that interest rates can be higher, often ranging from 25% to 49.9% APR for those with lower scores. If you only need a small sum for a quick fix, you can learn more about short term loans for smaller, urgent home repairs.

When to Consider a Secured Homeowner Loan

Secured loans suit large-scale projects like extensions or loft conversions. They allow you to borrow larger amounts over longer periods, which can lower your monthly outgoings. Some families also look into Lendology council-funded loans, which offer a social-lending model for homeowners. You must be cautious, though. Your home is at risk of repossession if you fail to keep up repayments on a secured debt. If you’re ready to see which path fits your budget, you can start your enquiry today to compare available lenders.

How to Apply for a Renovation Loan via Pixie Loans

Applying for a home improvement loan for bad credit doesn’t have to be a confusing chore. When you use a broker, the entire journey is organised to save you time. You can complete the initial enquiry form in just a few minutes using your phone or computer. The broker does the heavy lifting by searching multiple specialist lenders for you at once. With the Bank of England base rate currently at 3.75%, lenders are carefully balancing interest rates for new products. This system uses soft searches where possible to protect your score.

Step-by-Step Guide to the Application Process

The process for finding a home improvement loan for bad credit is straightforward and transparent.

- Step 1: Fill out the application form with your basic personal and financial details.

- Step 2: Review the loan offers from lenders who have indicated they are likely to accept you.

- Step 3: Complete the final application with your chosen lender to receive your funds.

A June 2026 report by the FCA highlights new proposals that give lenders more flexibility when assessing your affordability. This ensures you get a fair decision.

What Happens After Your Application is Accepted?

Once approved, the funds are typically transferred directly into your UK bank account. You can then begin your home improvements immediately, whether that involves hiring a builder or buying materials for a DIY project. If your repair is urgent, you should check your emergency loan eligibility first. Data from the ONS shows that the current UK inflation rate is 2.8%, so starting your project sooner may help you avoid rising costs for construction materials and labour. This helps you get the best value from your loan.

Take Control of Your Home Renovation Today

Renovating your property is a powerful way to increase its value and your daily comfort. Even with a poor history, securing a home improvement loan for bad credit is possible by highlighting your current disposable income. Lenders now use more holistic checks, as seen in recent FCA regulatory updates from June 2026. Using a broker allows you to access a panel of specialist lenders who look at your ability to pay today. This approach protects your credit score whilst helping you find a fair deal for essential repairs.

We act as a responsible guide to help you find suitable solutions. As an FCA-regulated UK credit broker, we match you with lenders who specialise in bad credit. Our simple online application process is transparent and supportive. You can also visit MoneyHelper for free, impartial guidance on managing your household budget. Don’t let past financial hurdles stop you from fixing your home. If you’re ready to transform your living space, apply for a home improvement loan for bad credit today.

Frequently Asked Questions

Can I get a home improvement loan for bad credit without a guarantor?

Yes, you can obtain a home improvement loan for bad credit without a guarantor. Many specialist lenders provide unsecured options where the decision is based on your current budget and monthly affordability. Whilst a guarantor can sometimes improve your chances of a better rate, it isn’t a mandatory requirement for every product. This allows you to maintain financial independence whilst funding your essential property repairs.

Will applying for a renovation loan through a broker hurt my credit score?

Applying through a broker usually starts with a soft credit search, which has no impact on your credit score. This process allows multiple lenders to review your eligibility without leaving a permanent mark on your record. Other lenders won’t see these initial enquiries. You’ll only face a hard search once you decide to move forward with a specific loan offer from a chosen lender.

How much can I borrow for home improvements with a poor credit history?

Borrowing limits vary, but many unsecured products for poor credit range from £100 up to £5,000. If you require a larger sum for a major project, you may need to consider a secured loan. Lenders calculate your specific limit by looking at your monthly wages and outgoings. They want to ensure that the repayments remain manageable within your current lifestyle and don’t cause financial strain.

Can tenants apply for home improvement loans or is it only for homeowners?

Tenants are eligible for unsecured loans, though they cannot access secured homeowner products. If you rent your home, you can use these funds for portable upgrades like new appliances or removable flooring. It’s vital to check your tenancy agreement first. Most landlords require written consent before you carry out any significant work, even if you are paying for the improvements yourself.

How long does it take to get the money for my home repairs?

You can often receive the funds within the hour if you choose an unsecured loan and are approved quickly. The online matching phase takes just minutes to complete. However, if you opt for a secured loan, expect the process to take several weeks. This is because lenders must conduct a professional valuation of your property and perform detailed legal checks before releasing any money.